CBEC Sets up 23

Excise Zones for Audit Commissionerates, Issues

Guidelines

[CBEC Circular No. 985 dated 22nd September

2014]

Subject – Guidelines regarding Structure,

Administrative set up and Functions of Audit Commissionerates.

On implementation of cadre review there would be 23

Central Excise Zones and 4 Service Tax Zones with each zone having one or more

Audit Commissionerates. Each Audit Commissionerate would cover assessees

registered under the jurisdiction of 3 to 5 Executive Commissionerates.

Principal Chief Commissioner and Chief Commissioner shall assign the

jurisdiction of Audit Commissioner in the zone, decide

the location of Audit Commissionerates and its

subordinate offices. Following guidelines may be followed while finalizing the

location and organizational structure of Audit Commissionerate

and its subordinate offices, subject to deviations needed to cater to the local

requirements.

Location of Audit Commissionerate

2.1 The

headquarters and the subordinate offices of the Audit Commissionerates

could be co-located in metropolitan city based zones.

2.2 In

non-metropolitan city based zones, Executive Commissionerates

are spread over different cities therefore the headquarters of the Audit Commissionerates may be located in the city where zonal

office is located, and at least one of the Circles (subordinate office

explained later) may be located in the city where Executive Commissionerates

are located.

2.3 In cases

where there is more than one Audit Commissionerate in

the Zone, the location of the second or third Audit Commissionerate

and its subordinate offices may be decided based on the geographical

concentration of the taxpayers. However, the Headquarters of the Audit Commissionerate may be in the city where the Executive Commissionerate is located. This is to ensure that audit

officers work in close coordination with the Executive Commissionerates

and are accessible to the assessees.

2.4 LTU Audit -

Two LTU Audit Commissionerates have been created. LTU

Audit Commissionerate at Delhi shall have

jurisdiction over assessees registered with LTU

Delhi, Kolkata or Bangalore whereas LTU Audit Commissionerate

at Mumbai shall have jurisdiction over the assessees

registered with LTU Mumbai or Chennai. The assigning of audit to the

subordinate offices of these Commissionerates may be

carried out taking into account the location of cluster of assesses. While

assigning assessees to the subordinate office, assessees with same PAN number should be assigned to one

subordinate officer.

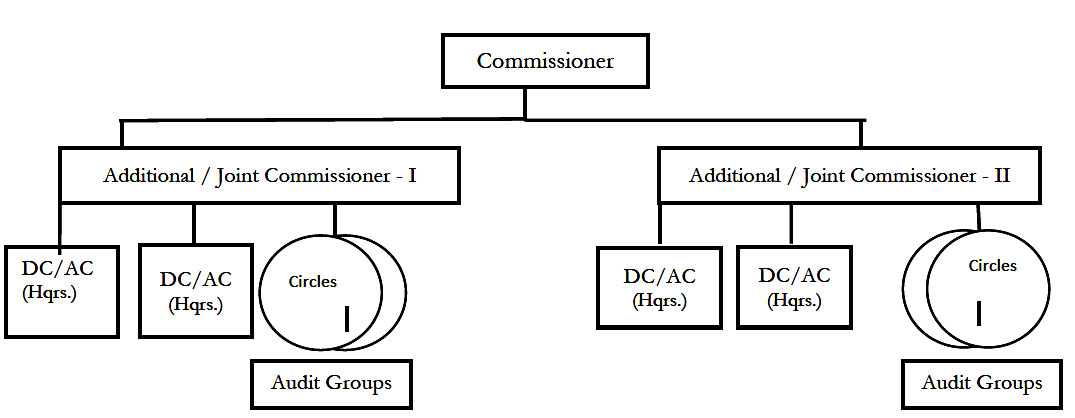

Configuration of Audit Commissionerate

3.1 Audit Commissionerate would comprise of a Headquarters similar to

an Executive Commissionerate and subordinate offices

proposed to be called Circles similar to a Divisions. The Circles would be

headed by a Deputy or Assistant Commissioner. The Circles would comprise of

Audit Groups equivalent to the Range offices which would have Superintendents

and Inspectors.

3.2 Audit

Commissioner would be Head of the Department and the headquarters would have

two Additional or Joint Commissioners, who are in turn would be supported by

two Deputy or Assistant Commissioners each.

3.3 The proposed

sections in the Headquarters are:

i. Planning and coordination section to look after scheduling and

support in conduct of MCM meeting, maintenance and updation

of Assessee Master File, maintenance of

Records/Registers and submission of reports to look after formation /

constitution of audit groups and deployment of officers matching skills with

audit requirement, maintenance of database of officer’s profile, training needs

of officers.

ii. Administration,

Personnel & Vigilance section to look after administrative matters,

transfer, leave, allowances, budgetary grants, vigilance matters etc.

iii. Technical section

to look after draft Show Cause Notices, audit follow up, court cases, Board’s

circulars, instructions etc.

iv. Risk Management

and Quality Assurance section to look after risk based selection of units, use

of Third Party Source of Information, maintenance of Audit database of units to

be audited, selecting themes/issues for audit, performance appraisal and

Quality Assurance

3.4 The aforementioned four sections of an Audit Commissionerate

can be manned by either 3 or 4 Deputy / Assistant Commissioners in the

Headquarters. In case of three Sections in Headquarters, the Technical and

Planning function can merge into one. The other Deputy / Assistant

Commissioners would be in charge of Circles. Each Audit Commissionerate

may have 6 to 7 Circles under its jurisdiction.

3.5 The Circles would

be assigned the geographical jurisdiction of either an entire Commissionerate or some Divisions of an Executive Commissionerate.

3.6 Division of

the jurisdiction of an Executive Commissionerate

between two Audit Commissionerates / Audit circles

should be avoided.

3.7 In addition

to geographically defined Circles, the Audit Commissionerates

may have functionally oriented Circles for conducting Theme/Issue based audit

(for example Insurance, telecom, Banking services or specific commodities etc) and its territorial jurisdiction should cover the

jurisdiction of the entire Audit Commissionerate.

Organisational Structure of Audit Commissionerates

Staffing norms

4.1 Headquarters

shall be manned by one Commissioner, two Additional or Joint Commissioners and three

or four Deputy Commissioners.

4.2 Each Audit

Circle shall be headed by Deputy or Assistant Commissioner and will also

comprise of Audit Groups. The Audit Groups deployed for large units should

comprise of 2-3 Superintendents and 4-6 Inspectors. For Medium units the Audit

Group should include 1 - 2 Superintendents and 2 - 4 Inspectors. For Small

units the Audit Group should include, 1 Superintendent

and 1 - 2 Inspectors.

4.3 Groups for

Large units, Medium units and Small units should be in such number that the

following distribution of manpower deploymentin audit

groups is achieved.

a. 50% of manpower to Large units

b. 30% of manpower to Medium units

c. 10 % of manpower to Small units

d. 10% of manpower for planning, coordination and follow

up.

Functions of Audit Commissionerate

5.1 Monitoring

Committee Meeting (MCM) should be convened by Audit Commissionerate,

for which the Executive Commissioner or his representative will be invited to

attend. The decision with regard to settlement of an audit objections

after recovery of all dues or dropping of the unsustainable audit objections

shall vest with the Audit Commissioner. Approved audit objections including

those in which show cause notices are proposed to be issued should be conveyed

to the Executive Commissioner in the form of Minutes of the MCMs, who shall

respond to these objections conveying his agreement/disagreement within 15 days

of the receipt of the minutes of the MCM.

5.2 On points of

difference, further consultations may be held for a maximum period of 15 days.

In case the difference persists, the final decision to issue show cause notice

rests with the Audit Commissioner.

5.3 Audit Commissionerate shall issue the show cause notice, wherever

necessary, after the audit objections are confirmed in the MCMs. The show cause

notice shall be answerable to and adjudicated by the Executive Commissioner or

the subordinate officers of the Executive Commissionerate

as per the adjudication limits prescribed the Board. Audit function will end

with the issuance of show cause notice and further action including

adjudication and follow-up shall be the responsibility of Executive

Commissioner.

5.4 Litigation

after adjudication proceedings (including defending the order before the

appellate forums-Commissioner (Appeals)/Tribunals/Courts) shall be the

responsibility of Executive Commissioner. However, Audit Commissionerates

shall remain closely associated and provide inputs wherever required.

5.5 The function

of pre-audit/post-audits of refunds, rebates and brand rate fixation of

drawback shall continue with the jurisdictional Executive Commissionerate.

5.6 CERA audit

shall be attended by the Executive Commissionerate by

compiling necessary information and replying to the audit objections raised by

C&AG. Audit Commissioners will have no role either in compiling /

furnishing information to CERA or replying to the C&AG objections. However,

it is desirable that Audit Commissionerate is aware

of the objections raised by C&AG. Therefore, copy of the objections received

from CERA and replies furnished by the Executive Commissioner shall be

forwarded to the Audit Commissionerate by the

Executive Commissionerate.

5.7 Anti-evasion

functions shall continue with the Executive Commissionerates.

Audit Commissionerates may refer, with the approval

of the MCM, any case arising out of audit where detailed investigation is

necessary to the Executive Commissionerates.

5.8 Special

Audit shall be ordered by the Audit Commissionerates.

Section 14A / 14AA of CEA, 1944 and Section 72A of the Finance Act, 1994

provide for such special audits in the specified circumstances by Cost

Accountants / Chartered Accountants. The Audit Commissioners shall be the

competent authority to order Special Audit, either on their own satisfaction or

on a reference received from the Executive Commissioner.

5.9 Audit should

be so conducted that the assessee is least

inconvenienced. Documents as prescribed in the manual should be called and

preparatory work finalized ahead of audit. Audit should be completed

expeditiously and as soon as the Final Audit Report is prepared , it should

be ensured that a copy of the Final Audit Report including ‘NIL’ report is

dispatched or provided to the assessee under

acknowledgement to be kept in Assessee Master File.

5.10 Currently,

audit is undertaken for each tax separately even though the business and

financial records verified during the audit remains common for all the three

tax administered by the Board . In order to improve the efficiency of audit

process, it has been decided that coordinated and integrated audit covering two

or more taxes for assessees having common PAN shall

be carried out. Necessary legal enablement has been provided in the

notification conferring territorial jurisdiction to the Commissionerates

such that Service Tax Audit Commissionerates can

audit Central Excise assessees within a zone and

vice-versa. An assessee who is registered under

Central Excise, Service Tax and Customs need not be subjected to three separate

audits. The information about his various registrations is available and such assessees would be subjected to a complete audit by the

designated Audit Commissionerate. For this purpose

the Principal Chief Commissioner / Chief Commissioner will assign the audit of

an assessee to a particular Audit Commissionerate,

based on payment of Central Excise duty or Service tax whichever is higher.

Following the same principle OSPCA would be also be carried out by the

designated Central Excise or Service Tax Audit Commissionerate,

in an integrated manner.

5.11 It is

proposed to issue risk based audit norms in due course of time. In the interim

the existing audit norms may be used to ensure that audit functions continue

efficiently.

Transfer policy and capacity building

6.0 Audit

requires specialized skills in accountancy and handling of financial / SAP or

ERP related databases apart from domain knowledge of Central Excise, Service

Tax and Customs law and procedures. The officers need to gain knowledge of

compliance requirements under Income Tax, Companies Act, VAT laws to do a

comprehensive and meaningful audit. The officers who have gained expertise in

this regard are few. DG (Audit) in consultation with NACEN shall develop

appropriate modules for training of officers in audit functions and inform field

on further progress. As it takes time for officers to gain expertise in audit

techniques , appropriate transfer policy to be followed by Zones shall be

prepared by the DG, Audit with due approval of the Board so that the

department can adequately use officers for audit after they have acquired the

necessary skills . Suggested transfer policy shall be circulated by the DG , Audit after approval of the Board .

Removal of difficulty

7.0 Past

guidelines and instructions on the subject stand modified to the extent they

are in conflict with these guidelines . If there is

any difficulty in implementing the above guidelines , Principal Chief

Commissioners and Chief Commissioners are authorised

to issue appropriate instructions to be valid for temporary periods to remove

difficulty in setting up and operationalizing Audit Commissionerates . Issues which need to be addressed in the

Board may be forwarded to the Director General of Audit with suggestions for

further examination and seeking approval of the Board where needed .

[F.No. 206/03/2014-CX.6]