Chennai

Customs Denies Duty Free Import from LDC Country due to Third Country Invoicing

Speaking Order for Denial of Duty

Free Tariff Preference for Least Developed countries Scheme notified vide Notification

96/2008 dated 13.08.2008 in accordance with the provisions of Rules of Origin

published vide Notification No. 29/2015-Customs Tariff (Determination of Origin

of Products under the Duty Free Tariff Preference Scheme for Least Developed

Countries) Rules, 2015

[Ref: Chennai Customs F.No. S.Misc. 546/2020-Gr.2 dated

17.11.2020]

The

Chennai based Importer imported Teak Sawn Timber from Togo under duty free

import from LDC countries. The goods were imported from Togo while the purchase

invoice was issued from UAE.

Under

Free Trade Agreement and importing under FTA countries, the provisions of rule

of origin must be compatible. In this case the Customs official denied duty

free rule of origin benefit due to third country invoice.

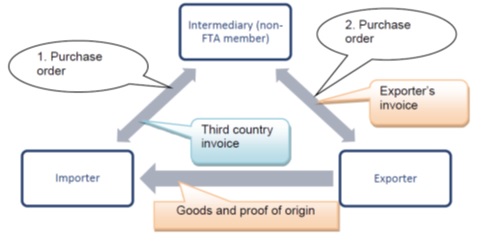

The

practice of Third country invoice is common in international trade to

involve an intermediary between the importer and the exporter. An extract from

World Customs Organisation (WCO) guidelines is giving

below.

Extract

from WCO Guidelines on Certification of Origin

Third country invoice (intermediary

trade)

It

is a common practice in today’s international trade to involve an intermediary

between the importer and the exporter. This practice must be recognized and the

related procedures must be in place. In trade involving an intermediary

residing in a third country, the invoice issued in the third country (a third

country invoice) would be submitted to the Customs of the importing country to

support the import declaration.

In

the case where third country invoicing is involved, the following guidelines

are provided to ensure the appropriate processing of intermediary trade.

Guideline:

(INTERMEDIARY

TRADE)

8.

Recognizing the current practices of trade, a proof of origin issued in the

country of origin should be accepted in cases where the commercial invoice is

issued in a third country, as long as it is discernible that the goods referred

to in the proof of origin and the invoice corresponds to each other and that

the goods satisfy the applicable rules of origin.

9.

When a declaration of origin is issued by an approved exporter for goods which

are traded via an intermediary business based in a third country, the

declaration of origin should be made out on a commercial document other than an

invoice1 which the approved exporter

issues on his/her own responsibility and which clearly identified the goods it

accompanies.