China Gains $460bn from

Commodity Slump

Picnic Over, Prices Rising Again

China got a $460 billion break

annually during the collapse in commodity costs, so this year’s rally in

everything from oil to iron ore is starting to erode the bonus of cheap

imports.

Rising prices take money from consumers who use

more food, energy and metals than any others in the world. It also increases

inflationary pressure, limiting the scope of the country’s central bank to

stimulate the economy through further monetary easing.

“Any significant upturn in commodity prices such as

oil and gas and iron ore would therefore have a net negative impact on the

Chinese economy,” Rajiv Biswas, Asia-Pacific Chief Economist at IHS Global

Insight, said in an e-mail.

Base metals like zinc and copper are off to their

best start since 2012, crude is set for its biggest monthly gain in almost a

year, and iron ore used to make steel has surged into a bull market after

touching a record low in December. While domestic producers of those raw

materials benefit, China is a net importer, so those gains mean higher costs

and more pressure on profit margins for industries already struggling with

slowing growth.

The following charts illustrate some of the costs

and benefits of the fledgling recovery in commodities for China.

Crude oil’s 35 percent plunge last year saved China

about $320 billion. The rest of the savings came from metals, coal and

agricultural commodities. The country gets about 60 percent of the oil it needs

from overseas. With prices slumping as low as $27 a barrel this year, refiners

have been on a massive buying spree, importing record amounts and filling

strategic stockpiles to an estimated 80 percent of operational capacity.

Prices have rallied more than 40 percent, near $40,

which may reduce China’s overall commodity bonus to about $440 billion on an

annual basis. While that reduction has little impact on the economy, prices

sustained at $55 to $60 would start to generate more serious headwinds, he

said. China would probably slow purchases if oil topped $70.

The rally isn’t all bad for China, partly because

it would increase the value of the inventory stockpiled when prices were lower.

Oil at $40 also helps the cash flow of domestic producers including PetroChina Co. and Cnooc Ltd.,

who have cut production because most need prices at about $50 to break even.

China’s steel mills lost money for most of last

year, even as the cost of iron ore plunged, because of a global glut and

weak demand. Now, iron

ore has surged 21 percent this year, including an unprecedented 19 percent jump

on March 7 to an eight-month high of $63.74 a metric ton. That’s putting more

pressure on an industry already battered by the worst margins since at least

2007. After years of economic expansion, China has more than 400 million tons

of surplus steel capacity.

The degree of pain from more-expensive iron ore

depends on whether steel prices can keep pace. Spot rebar in China has risen

about 18 percent this year, helping lift margins into positive territory for

the first time since May. An improvement in profits may encourage some

shuttered plants to resume output.

Prolonging the life of unprofitable mills is going

to complicate the government’s efforts to restructure the industry by closing

some down, though it would be good news for the 500,000 workers whose jobs are

at risk.

Either way, the recovery will be a boon to domestic

iron-ore mines hurt by a flood of cheap supplies from Australia and Brazil,

provided the rally lasts. Many, from Goldman Sachs Group Inc. to China Iron

& Steel Association, say this year’s price jump is a blip that isn’t

sustainable. According to the median of nine estimates in a Bloomberg survey,

prices will return to $41 in the second quarter.

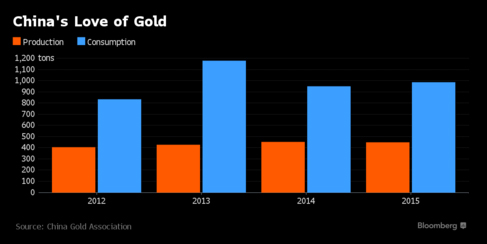

China’s

been buying gold in a big way, including during the precious metal’s three-year

slump through 2015. This year, prices are up 16 percent, touching a 13-month

high of $1,284.64 an ounce on March 11. In July, the central bank disclosed

that it had expanded gold holdings by 57 percent in six years as the nation

sought to diversify its foreign exchange reserves. The People’s Bank of China

has increased its hoard every month since then, and it reached about 1,788 tons

by the end of February. This year’s advance in bullion -- the best performance

of any raw material on the Bloomberg Commodity Index -- has increased the value

of those assets.

Only

about 2 percent of China’s reserves are in gold, compared with 67 percent for

Germany and 73 percent in the U.S., according to data from the World Gold

Council.

Last year,

China was the world’s largest consumer of gold jewelry at 783.5 tons, compared

with 654.3 tons bought by Indians. While the price rebound is going to make

everything from rings to necklaces more expensive, it’s a boon for miners in

what’s also the world’s biggest producing country. Zijin

Mining Group Co. shares have climbed 23 percent this year in Hong Kong after

losing 7.7 percent in 2015.