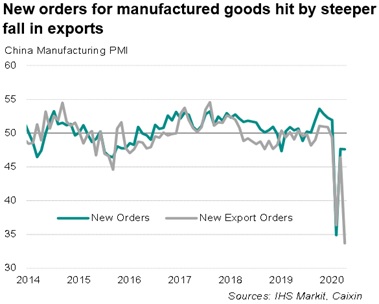

China’s

New Export Orders Index at 33.5 – Container Shipping Demand in Free Fall

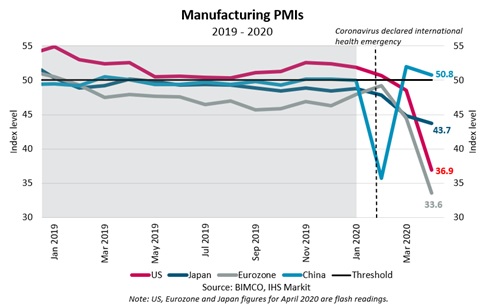

Global economic activity continues to suffer

as the coronavirus runs rampant and manufacturing PMI readings for April indicate

a massive weakening of global manufacturing. While flash readings in the US and

Eurozone composites declined to 36.9 and 33.6 index points respectively, the

flash reading in Japan showed surprising resilience, declining only 1.1 points

to 43.7 index points in April. Nonetheless, the readings reveal deep

contraction which will result in choppy seas in the coming months, particularly

for container shipping.

China’s manufacturing PMIs in April

highlighted sluggish recovery from March. The PMI figure from Caixin highlighted a contraction to 49.4 index points,

while the figure from the National Bureau of Statistics China (NBS) showed an

expansion to 50.8 index points.

The common denominator between the two was the

New Export Orders sub index (at 33.5 points), which in both cases plummeted

amid slowing demand from the rest of the world.

US retail sales at clothing stores halved in

March

Global manufacturing activity is slowing on

the back of the constrained labour force and

faltering demand, and data from the US Census Bureau highlight how US retail

sales effectively slammed into a brick wall in March 2020. As the US entered a

state of lockdown in March, clothing and clothing accessories stores saw retail

sales drop 50% from February 2020 as well as year-on-year.

Similarly, sales in furniture stores dropped

26.8% from February, while motor vehicle and parts dealers had their sales

slashed by 25.6%, also compared with February. The products and parts sold in

these types of stores constitute a significant fraction of all seaborne containerised goods, and such dramatic drops in US retail

sales are indicative of the calamity that container carriers face.

Manufacturing PMIs slide into unparalleled

contraction

In Japan and the Eurozone, the manufacturing

PMIs have been in contraction since February 2019, while the US remained in

expansion until March 2020. With all the readings now in unprecedented

contractionary territory, and the US and Eurozone seeing the largest declines

on record, dwarfing the impact of the financial crisis, a gloomy path lies

ahead. The slowing new orders domestically, as well as for exports and

diminishing backlogs, amplifies the bleak outlook for the foreseeable future.

While PMI readings could quickly be back above

50 index points, it does not imply a return to pre-crisis conditions, but

rather, a slight improvement from last month’s activity level. It is important

to note that structural damage has already been inflicted on economies around

the world, including massive rises in unemployment which will protract any

recovery to normal conditions.

Container carriers will be stress-tested in

the coming months

Manufacturing PMI readings serve as a

bellwether for container shipping volumes for the months ahead, and recent data

suggest that 2020 will be a stress-test for container carriers, perhaps on an

unprecedented scale.

Idle container ship capacity ticked up when

Chinese lockdowns created export disruptions in February, and idle container

capacity remain around 10% of the total fleet as demand for containerised

goods in advanced economies fade. Supply chain disruptions are on retreat,

which is certainly a positive development, but with slowing consumer demand for

finished goods, seaborne container volumes are set to remain low and outright

decline in 2020.

In recent years, the container shipping

industry has been battling challenging market conditions, squeezing container

carriers’ operating margins. 2019 marked, for a change, a full year of

profitability judged by the average operating margins for main carriers

(source: Alphaliner). Yet, faced with the greatest

economic downturn since the Great Depression during the 1930s, any profits of

recent years could be wiped out in a matter of months.

[Source: Peter Sand, Chief Shipping Analyst,

BIMCO BIMCO]