Direct Tax Vivad se Vishwas Act, 2020

Timelines Extended to 30 June 2021 from 30 Apr 2021

·

Sec. 153 or Sec. 153B

·

Sec.144c(13)

·

Sec. 148

·

Sec. 168(1) – Processing of Equalisation

Levy

In view of the severe

Covid-19 pandemic raging unabated across the country affecting the lives of our

people, and in view of requests received from taxpayers, tax consultants &

other stakeholders that various time barring dates, which were earlier extended

to 30th April, 2021 by various notifications, as well as under the Direct Tax Vivad se Vishwas Act, 2020, may

be further extended, the Government has extended certain timelines on 24 April

2021.

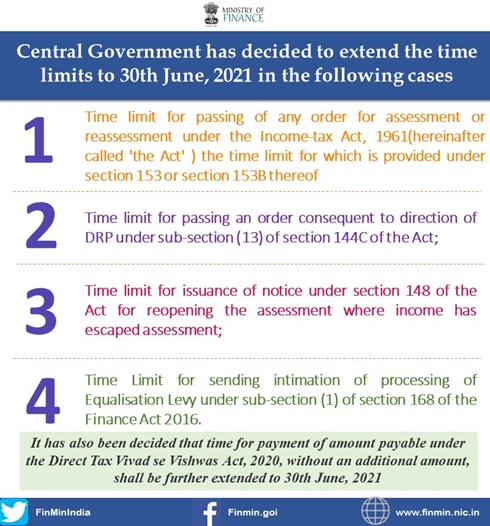

In the light of several

representations received(supra) and to address the hardship being faced by

various stakeholders, the Central Government has decided to extend the time

limits to 30th June, 2021 in the following cases where the time limit was earlier

extended to 30th, April 2021 through various notifications issued under the

Taxation and Other Laws (Relaxation) and Amendment of Certain Provisions Act,

2020, namely:-

(i) Time limit for

passing of any order for assessment or reassessment under the Income-tax Act,

1961(hereinafter called 'the Act' ) the time limit for which is provided under

section 153 or section 153B thereof;

(ii) Time limit for passing an order

consequent to direction of DRP under sub-section (13) of section 144C of the

Act;

(iii) Time limit for issuance of notice under

section 148 of the Act for reopening the assessment where income has escaped

assessment;

(iv) Time Limit for sending intimation of processing of Equalisation

Levy under sub-section (1) of section 168 of the Finance Act 2016.

It has also been decided that time for payment

of amount payable under the Direct Tax Vivad se Vishwas Act, 2020, without an additional amount, shall be

further extended to 30th June, 2021.

Notifications to extend the above dates shall

be issued in due course.