Global Imports of Seaborne Wheat maintain Upward Trend

·

India

not in the Picture

·

Prices also eased as

maritime exports from Ukraine resumed following agreement on the Black Sea

Grain Initiative, which was signed in July 2022 under the auspices of the

United Nations and Türkiye.

By Emmanuelle Ganne (WTO), Alexander Karavaytsev (International Grains Council — IGC), Mun How

Mong (WTO), Cédric Pene (WTO)

Wheat

is among the world’s most common food staples. Its availability is therefore

crucial for food security in many parts of the globe. While around one-quarter

of the world’s wheat supply is obtained through international trade — 80 per

cent of it seaborne trade — this share is much higher for some net

food-importing developing economies. This highlights how important it is for

international trade channels to function well.

A new dashboard to log wheat maritime trade and food security

The WTO

and the International Grains Council (IGC) have jointly developed a new dashboard

to allow users to monitor short-term trends in maritime wheat flows. This

information is particularly important at a time when concerns about food

security and risks of supply chain disruptions are so high on the agenda.

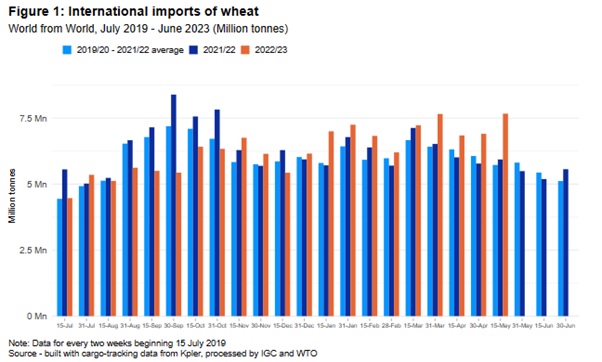

Data on global seaborne wheat shipments

The

latest data reveals that seaborne shipments of wheat continued at a strong pace

in the second half of May 2023, with arrivals at monitored ports estimated at

around 7.7 million tonnes. This is 40 per cent higher than the same period last

year and one-third higher than the three-year average.

Around

6.5 million tonnes of wheat were dispatched over the last 14 days. Taking into

account volumes of wheat in transit as of 4 June (4.2 million tonnes), Russia,

with close to 3 million tonnes, was the world’s largest wheat exporter,

followed by Australia, with over 2 million tonnes, Canada (1.4m), the United

States (0.8m), Ukraine (0.5m) and France (0.4m). China, Indonesia, Algeria,

Egypt and Spain are the key destinations in order of volume for these exports

(as of 4 June).

After a

relatively slow start to the July 2022 – June 2023 season due partly to

disruptions caused by the outbreak of the war in Ukraine, global maritime trade

flows accelerated in late 2022 as global prices retreated as a result of

improving global wheat availability and stiff competition for export business.

Prices also eased as maritime exports from Ukraine resumed following agreement

on the Black Sea Grain Initiative, which was signed in July 2022 under the

auspices of the United Nations and Türkiye.

Cumulative

2022-23 global seaborne imports of wheat were around 140 million tonnes by the

end of 2023, marginally higher than the volume during the same period the

previous year, and 5 per cent higher than the average volume over the past

three seasons.

However,

parts of Africa, Southern and South-eastern Asia as well as the Caribbean and

South America have seen a decline in imports while imports to Western and

Eastern Asia, Northern Africa, Europe and Oceania have increased.

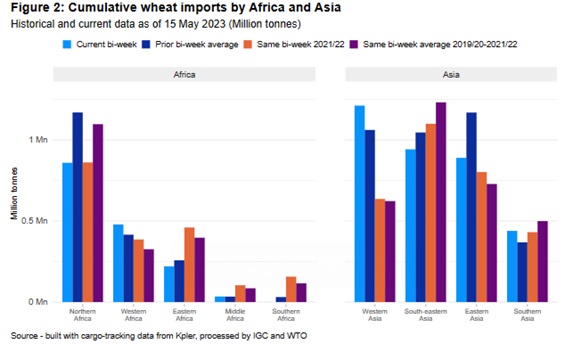

Contrasts in deliveries to Africa and Asia

In

Northern Africa, disappointing harvests in some countries reduced domestic

wheat availability, underpinning imports across the region in May. Deliveries

in the second half of the month were estimated at 1.9 million tonnes — almost

double the import levels during the same period one year ago. For the marketing

year (July-June), the cumulative total through May stands at around 29 million

tonnes, up by 9 per cent year-on-year, with smaller year-on-year imports by

Egypt outweighed by larger arrivals in other countries in the region, notably

Algeria, Morocco and Tunisia.

Wheat

imports by Western Asia have also been exceptionally strong, with cumulative

deliveries through the end of May 42 per cent above the average level over the

same period and one-quarter higher than last season. This trend is expected to

continue in the coming weeks. Of the 8.6 million tonnes of wheat in transit to

monitored ports around the world as of the end of May, with a significant

portion originating from Russia, the bulk was destined for Western Asia (1.7

million tonnes) and Northern Africa (1.6 million tonnes).

In

contrast, wheat deliveries to Western, Eastern and Central Africa are lagging

well behind those for last season and the average pace of exports. In Eastern

Africa, the bulk of the year-on-year decline stems from lower deliveries to

Djibouti, the major portion of which is assumed to be transhipped to Ethiopia,

where import needs this season are likely capped by a good local crop.

Accumulated deliveries to Madagascar, Réunion and Kenya are also lower than

last season but those to Somalia and Tanzania are up slightly. In Western

Africa, reduced imports by Nigeria, Ghana, Liberia and Togo outweigh larger

deliveries to Côte d’Ivoire and Guinea.

Deliveries

to Southern Asia have been generally slow this season, in part owing to smaller

deliveries to Iran, where long delays at discharge were also reported in recent

months. Cumulative arrivals in the region lagged last season by one-quarter as

of the end of May.

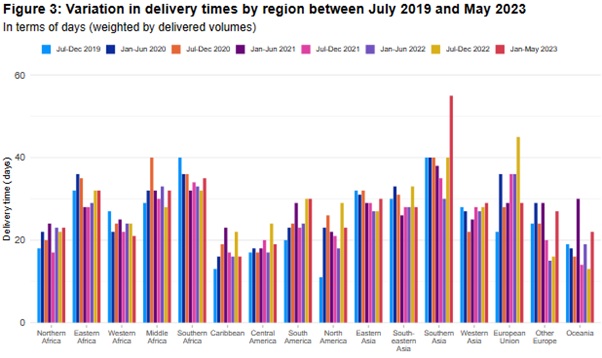

Delivery times to some regions have increased

In the

period from July 2022 to May 2023, calculated delivery times (from dispatch to

unloading) took markedly longer to reach monitored regions than they did during

the previous season (July-June), with regions such as Eastern Africa, Central

America, South America, Eastern Asia, Other Europe and Southern Asia especially

affected. For Southern Asia, delivery times in the July 2022 — May 2023 period

averaged 46 days, up from 33 days during the prior season — a relatively steep

increase stemming partly from longer delivery times to Iran.

South-Eastern

Asia and Central Africa have some of the longest average delivery times.

The

wheat maritime trade and food security dashboard provides aggregated estimates

for seaborne wheat shipments based on private vessel tracking, compiled by Kpler, a commodities market data and analytics solutions

company. Data are updated twice a month, in the middle and at the end of each

month.

In

addition, two live dashboards, which are updated every three hours, enable

users to visualize the short-term evolution of trade in grains and oilseeds,

including wheat, as well as corn, barley and soybeans over the previous 14

days. These live dashboards will be discussed in a future blog post.