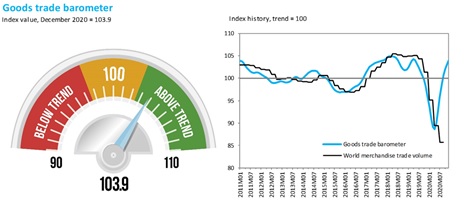

Goods Barometer Signals Strong Trade Rebound

but Momentum may be Short Lived

World merchandise trade volume growth remained strong in the

fourth quarter of 2020 after trade rebounded in the third quarter from a deep COVID-19

induced slump; however, the pace of expansion in the fourth quarter is unlikely

to be sustained in the first half of 2021 since key leading indicators appear to

have already peaked, according to the WTO’s latest Goods Trade Barometer of 18 February

2021.

The barometer's current reading of 103.9 is above both the baseline

value of 100 for the index and the previous reading of 100.7 from last November,

signalling a marked improvement in merchandise trade since

it dropped sharply in the first half of last year. All component indices are either

above trend or on trend, but some already show signs of deceleration while others

could turn down in the near future. Furthermore, the indicator may not fully reflect

resurgence of COVID-19 and the appearance of new variants of the disease, which

will undoubtedly weigh on goods trade in the first quarter of 2021.

Indices for export orders (103.4) and automotive products (99.8),

which are among the most reliable leading indicators for world trade, have both

peaked recently and started to lose momentum. In contrast, the container shipping

(107.3) and air freight (99.4) indices are both still rising, although higher-frequency

data suggest that container shipping has dipped since the start of the year. Finally, while the indices for electronic components

(105.1) and raw materials (106.9) are firmly above trend, this could reflect temporary

stockpiling of inventories. Taken together, these trends suggests that trade's upward

momentum may be about to peak if it has not already done so.

In the third quarter of 2020, the seasonally-adjusted volume

of world merchandise trade bounced back from a deep second quarter slump, boosted

by rising exports in Asia and increasing imports in North America and Europe. Goods

trade in the third quarter, nevertheless, was still down 5.6% compared to the same

period in 2019 after having falling 15.6% in the second quarter. These declines, while still very large, are less

severe than many analysts feared at the start of the pandemic.

The WTO's most recent trade forecast of 6 October 2020 predicted

a 9.2% drop in the volume of world merchandise trade in 2020, but the actual decline

may be slightly less severe.

Prospects for 2021 and beyond, moreover, are increasingly uncertain

due to the rising incidence of COVID-19 worldwide and the emergence of new variants

of the disease. Recovery will depend to a large extent on the effectiveness of vaccination

efforts. The WTO expects to release its next trade forecast in mid-April.

The full Goods Trade Barometer is available here.

Additional

context for the Goods Trade Barometer

Given the appearance of new sources of uncertainty related to

the COVID-19 pandemic, charts illustrating additional high-frequency statistics

are provided here to help readers better understand the current economic context.

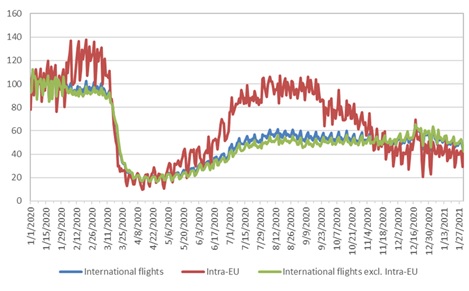

Chart 1: International

commercial flights, 1 January 2020 — 31 January 2021

(Index, week of 1 January = 100)

Source:

OpenSky Network and WTO Secretariat calculations.

Chart 1 shows international commercial flights per day (including

both passenger and cargo flights) recorded by the OpenSky

Network since 1 January 2020. Total flights rose towards the end of last year due

to holiday travel but have since fallen around 22% and currently stand at around

15% below their level in mid-August. Much of this fluctuation is due to intra-EU

flights, which have fallen more than 50% since mid-August, in part due to the resurgence

of COVID-19 and tighter restrictions on travel within Europe. Excluding intra-EU, international flights are

only down around 5% since last summer.

Chart 2: Number of daily

port calls of container ships, 1 January 2020 - 27 January 2021

(30-day moving average)

Source:

Cerdeiro, Komaromi, Liu and

Saeed (2020). Available at UN Comtrade Monitor.

Note: Based on Automatic Identification System (AIS) developed

by the International Maritime Organization (IMO) of the United Nations.

Chart 2 shows the number of daily port calls of container ships

since the beginning of 2020 recorded by the Automatic Identification System (AIS)

developed by the International Maritime Organization. Port calls in January were

down around 7% compared to December and 6% compared to the average of July-September

of last year. This suggests that the second

wave of COVID-19 will have an appreciable impact on shipments of goods by sea, which

is not yet fully reflected in the Goods Trade Barometer.

Chart 3: COMEX high grade

copper futures, 18 February 2020 — 16 February 2021

(US$ per pound)

Source:

Chicago Mercantile Exchange.

Prices of futures contracts for copper are a widely recognized

leading indicator of economic activity due to the importance of this metal in many

areas of manufacturing. Standardized contracts are traded on the COMEX exchange,

a division of the Chicago Mercantile Exchange (CME). Copper futures prices have

continued to climb in 2021 despite the ongoing pandemic and currently stand around

25% above their average level for the month of October 2020. This may reflect optimism about medium-term economic

prospects as effective vaccines are being distributed and as seasonal variation

may cause the number of COVID-19 cases to fall in the coming months. Given the importance

of Asia in global metals demand, it also reflects the comparatively better economic

performance and outlook for the region.

Chart 4: Visualization of phrases related to economic activity,

12 August 2019 - 31 January 2021

(% and index, neutral = 0)

Source:

The GDELT Project Summary Service.

The chart above shows the daily volume and average tone of news

reports containing phrases related to economic activity, as monitored by the GDELT

Project. The volume index has continued to decline while the tone index has remained

relatively positive since last November, both reflecting lesser concern about the

economic outlook than 6 to 9 months ago. This suggests that positive sentiment about

medium-term economic conditions, driven also by the arrival of vaccines against

COVID-19, may outweigh the negative impact of the still high number of COVID-19

cases worldwide.