India One of

the Worst Performer Among Global Exporters

· India

Exports Crash from $30bn per month to $20bn in Last Four Years as Economy Loses

Competitiveness

· WTO

Forecasts World Trade Growth to Fall by 1.1% to jest 1.7% in 2016

· 2017

may be a Repeat of 2016

· Contraction

driven by slowing GDP and trade growth in China and Brazil

· North

America, which had the strongest import growth of any region in 2014-15 too has

decelerated

World

trade will grow more slowly than expected in 2016, expanding by just 1.7%, well

below the April forecast of 2.8%, according to the latest WTO estimates. The

forecast for 2017 has also been revised, with trade now expected to grow

between 1.8% and 3.1%, down from 3.6% previously. With expected global GDP growth

of 2.2% in 2016, this year would mark the slowest pace of trade and output

growth since the financial crisis of 2009.

Main

Points

World

merchandise trade volume is expected to grow 1.7% in 2016, accompanied by real

GDP growth of 2.2% at market exchange rates. This would be the slowest pace of

trade and output growth since the financial crisis of 2009.

Trade

growth was weaker than expected in the first half of 2016 due to falling import

demand and slowing GDP growth in several major developing economies as well as

in North America.

Trade

in 2017 is expected to grow between 1.8% and 3.1%, a range being provided to

reflect potential changes in the relationship between trade and output.

Certain

trade-related indicators have improved, including export orders and container

port throughput, but overall momentum in trade remains weak.

The downgrade follows a sharper than expected decline

in merchandise trade volumes in the first quarter (-1.1% quarter-on-quarter, as

measured by the average of seasonally-adjusted exports and imports) and a

smaller than anticipated rebound in the second quarter (+0.3%).

The latest figures are a disappointing development and

underline a recent weakening in the relationship between trade and GDP growth.

Over the long term trade has typically grown at 1.5 times faster than GDP,

though in the 1990s world merchandise trade volume grew about twice as fast as

world real GDP at market exchange rates. In recent years however, the ratio has

slipped towards 1:1, below both the peak of the 1990’s and the long-term

average.

Falling

Commodity Prices

The

stagnation of world merchandise trade disguises strong shifts at the regional

level. There is the steep decline in imports of resource-exporting regions over

the last two years, driven by falling commodity prices and declining export

revenues.

Some

Hope

There

are some indications that trade may be picking up in the second half of 2016,

although the pace of expansion is likely to remain subdued. Container port

throughput has increased, export orders have risen in the United States, and

nominal trade flows in US dollar terms have stabilized, but numerous risks

remain.

The potential effects of the Brexit

vote in the United Kingdom has increased uncertainty about future trading

arrangements in Europe, a region where trade growth has been relatively strong.

Pound

Falls

The

UK referendum result did not produce an immediately observable downturn in

economic activity as measured by industrial production or employment; the main impact

was a 13% drop in the exchange rate of the pound against the US dollar and an

11% decline in its value against the euro. Effects over the longer term remain

to be seen. Economic forecasts for the UK in 2017 range from fairly optimistic

to quite pessimistic. Our forecast assumes an intermediate case, with a growth

slowdown next year but not an outright recession.

Exports of developed countries are expected to outpace

those of developing economies this year, 2.1% compared to 1.2%. On the import

side, developing countries are expected to register sluggish growth of 0.4%

compared to 2.6% for developed countries.

Imports

Crash in Latin America but Exports Pick Up

The biggest downward revision to imports from our April

forecast for 2016 applies to South America (-8.3% compared to -4.5% previously)

as the recession in Brazil intensified. This was followed by North America,

where import growth was revised down from 4.1% to 1.9% as GDP growth came in

below earlier projections. Asian import growth was also scaled back to 1.6%

from 3.2%, while our forecast for Europe was revised upward from 3.2% to 3.7%.

Export growth in 2016 was downgraded for most regions,

with the strongest revisions applied to Asia (0.3% compared to 3.4% in April)

and North America (0.7% compared to 3.1%). Meanwhile, South America’s export

growth is expected to be stronger than previously forecast (4.4% compared

1.9%), benefitting from favourable exchange rate

movements. Even with the downward revision to our estimates, risks to the

forecast remain mostly on the downside.

Contradiction

of Global Supply Chains, E-Commerce

A

number of reasons have been advanced to explain the decline in the ratio of

trade growth to GDP growth in recent years, including the changes in the import

content of demand, absence of trade liberalization, creeping protectionism, a

contraction of global value chains (GVCs), and possibly the increasing role of

the digital economy and e-commerce, but all have likely played a role. Whatever

the cause, the recent run of weak trade, and economic, growth suggests the need

for a better understanding of changing global economic relationships.

It

should be noted that the trade forecasts relate to changes in the quantity of

goods traded rather than changes in their dollar value. In 2015, merchandise

trade volumes continued to grow slowly despite the sharp 14% decline in the

dollar value of world trade, which was largely due to the appreciation of the

US dollar.

Volumes have grown but value

has fallen with dollar depreciation

Annual % change

|

|

2012 |

2013 |

2014 |

2015 |

2016P |

2017P |

|

|

Volume of world merchandise trade |

2.2 |

2.4 |

2.8 |

2.7 |

1.7 |

1.8 |

3.1 |

|

Exports |

|

|

|

|

|

|

|

|

North America |

4.5 |

2.8 |

4.1 |

0.8 |

0.7 |

1.6 |

2.9 |

|

South and Central America |

0.9 |

1.2 |

‐1.8 |

1.3 |

4.4 |

3.1 |

5.5 |

|

Europe |

0.8 |

1.7 |

2.0 |

3.7 |

2.8 |

1.8 |

3.1 |

|

Asia |

2.7 |

5.0 |

4.8 |

3.1 |

0.3 |

1.8 |

3.2 |

|

Other regions

a |

3.9 |

0.6 |

‐0.1 |

3.9 |

2.5 |

1.5 |

2.6 |

|

Imports |

|

|

|

|

|

|

|

|

North America |

3.2 |

1.2 |

4.7 |

6.5 |

1.9 |

1.9 |

3.1 |

|

South and Central America |

0.7 |

3.6 |

‐2.2 |

‐5.8 |

‐8.3 |

2.2 |

3.7 |

|

Europe |

‐1.8 |

‐0.3 |

3.2 |

4.3 |

3.7 |

1.8 |

3.1 |

|

Asia |

3.7 |

4.8 |

3.3 |

1.8 |

1.6 |

2.0 |

3.3 |

|

Other regions

a |

9.9 |

3.5 |

‐0.5 |

‐6.0 |

‐2.8 |

0.6 |

1.0 |

a Other regions comprise the Africa, Commonwealth of Independent States and Middle East.

Sources: WTO Secretariat for trade, concensus

estimates for GDP.

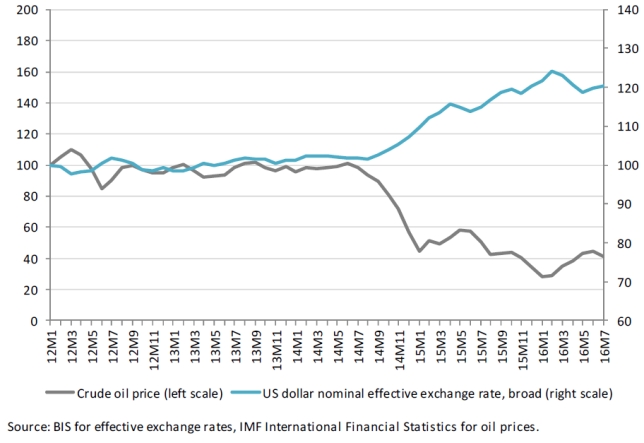

Dollar

Depreciates in 2016

As

chart below shows, the dollar has started to depreciate again in the first half

of 2016, with an inverse effect on values of traded goods, particularly

commodities such as oil. If this trend continues for the remainder of the year,

world merchandise trade growth in dollar terms could exceed trade growth in

volume terms in 2016. Trade developments in current dollar terms are shown for

selected economies.

Effective exchange rates

and crude oil prices, Jan. 2012 - Jul. 2016

(Indices, January

2012=100)

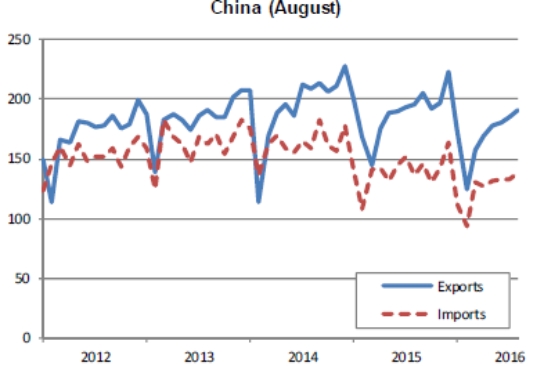

Merchandise exports and imports of selected

economies, January 2012-July 2016

(Billion dollars)