Nearly 26 lakhs GST Registered are Non-filers of GSTR 3B Returns, May

Face Cancellation of Registration

·

CBIC Asks Commissioners to Take Action

on Errants by 25 Nov

The Goods & Services Tax (GST) Administration plans

to act tough with non-filers of returns and cancel their registration. It has

also decided to update the progress made in this regard on a daily basis.

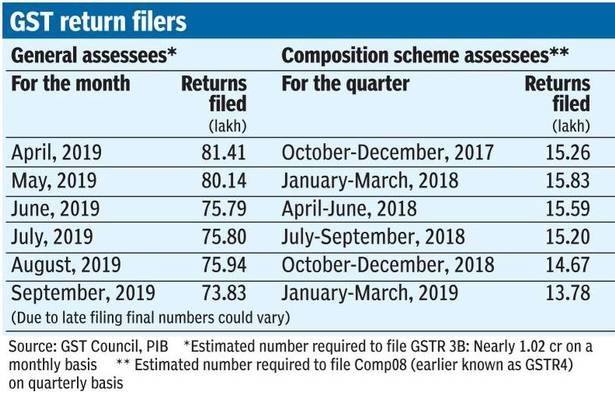

Filing of returns helps tax authorities to estimate the

tax liability and find out how much tax has been paid. The problem here is that

nearly 20 per cent of assessees do not file their

returns, which affects GST collections.

The Central Board of Indirect Taxes & Customs (CBIC)

held a meeting with the Principal Chief Commissioner and Commissioner of GST

& Customs on November 13. According to sources, PK Dash, Chairman, CBIC,

expressed his displeasure in the progress of cancellation of registration of

non-filers who have not filed GSTR 3B (showing tax payments) returns for six or

more than six return periods and are liable to action under GST law.

“…the task of

cancellation of registration of such non-filers of GST returns should be taken

on priority basis and should be furnished by November 25, ” a communication

sent from the office of the Principal Chief Commissioner of GST & Central

Excise, Mumbai to Principal Commissioner/Commissioner posted in its

jurisdiction. It has also asked for reports to be sent on a daily basis.

Conditions for Cancellation

Section 29 of the Central Goods & Services Tax (CGST)

Act prescribes conditions for cancellation of registration and fulfilment of

any of these will invite action. These include contravention of the provisions

of the Act, a composition scheme assessee not filing returns

for three consecutive tax periods, any non-composition assessee

not furnished returns for a continuous period of six months, not commencing

business within six month from the voluntary registration, and registration

obtained by means of fraud, wilful misstatement or

suppression of facts. The Act clearly provides that registration will not be

cancelled without giving the person an opportunity of being heard.

According to GST Law, a registered person will have to

file returns either monthly (normal supplier) or on a quarterly basis (supplier

opting for composition scheme). An ISD (Input Service Distributor) will have to

file monthly returns showing details of credit distributed during the

particular month. A person required to deduct tax (TDS or Tax Deducted at

Source) and persons required to collect tax (TCS or Tax Collected at Source)

will also have to file monthly returns showing the amount deducted/collected

and other specified details. A non-resident taxable person will also have to

file returns for the period of activity undertaken.

The law is very clear here that the cancellation of

registration will not affect the liability of the person to pay the tax and

other dues. Every registered person whose registration is cancelled will pay an

amount, by way of debit in the electronic credit ledger or electronic cash

ledger, equivalent to the credit of input tax in respect of inputs held in

stock and inputs contained in semi-finished or finished goods held in stock or

capital goods or plant and machinery on the day immediately preceding the date

of such cancellation or the output tax payable on such goods, whichever is

higher.