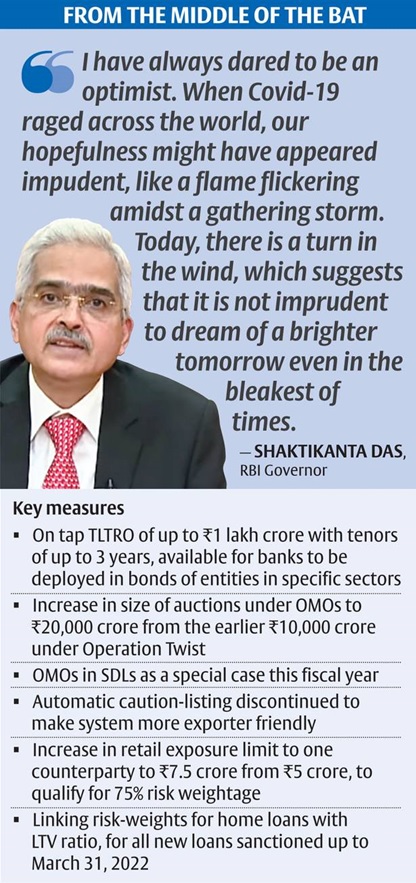

RBI Delivers

without a Policy Rate Cut

The slew of liquidity and financial market measures promises

pre-Diwali cheer

As

widely expected, the Monetary Policy Committee maintained status quo on the key

policy rate, with inflation rate holding above the RBI’s comfort level. But the

MPC brought pre-Diwali cheer by giving a ‘whatever it takes’ assurance to

revive growth, as it looked at the “current inflation hump as transient”.

The

5:1 vote of the six-member MPC in favour of a

continued accommodative stance “at least during the current financial year and

into the next financial year”, also offered markets an extended comfort on

rates and liquidity.

Key overhangs

The

policy had to address three key overhangs weighing on markets. One, the RBI’s

seemingly hardline stance on inflation, which has now eased with the current

narrative opening up scope for further rate cuts. Two, concerns over the RBI

reversing its liquidity stance to abate inflation worries. Three, the huge

oversupply of Central and State government bonds slated to hit the market

towards the end of the fiscal, exerting upward pressure on long-term bond

yields. The slew of liquidity and financial market measures announced by the

RBI considerably ease these concerns.

“The augmented borrowing programme for 2020-21 has been

necessitated due to the exigencies imposed by the pandemic in the form of the

fiscal stimulus and the loss of tax revenue. While this has imposed pressures

on the market in the form of expanded supply of paper, the RBI stands ready to

conduct market operations as required through a variety of instruments to

assuage these pressures, dispel any illiquidity in financial markets and

maintain orderly market conditions,” said RBI Governor Shaktikanta

Das.

SBI

Group’s Chief Economic Advisor Soumya Kanti Ghosh said: “Recourse to non-conventional policy

tools has been the most innovative tool that the RBI has been using to manage

financial stability in a most durable manner in the current challenging

circumstances. Accordingly, the adjustment in risk weights, OMO in SDL,

extension of co-origination model and enhanced HTM limits are measures that are

bold and pragmatic.”

While

conservatives will fret over both inflation and financial stability risks, Abheek Barua, Chief Economist,

HDFC Bank, believes that the RBI has not gone overboard in its effort to

support growth. “The Indian economy’s revival efforts are hobbled by the lack

of adequate fiscal support. If the monetary policy does have to do the heavy

lifting, it cannot do it within the confines of a conventional ‘take-no-risks’

framework,” he said.

“The

RBI,” said Ananth Narayan, Professor at SPJIMR, “has

managed the borrowing programme very well so far. The

big measures announced yesterday send a strong signal that the RBI will ensure

that yields are kept under check. Including T-bills, over ₹13-lakh

crore of central borrowing is already done. Hence, the real concern was with

SDLs, where only ₹3-lakh crore of borrowings

has been completed so far. The OMOs of SDLs is a welcome move that will address

the issue of oversupply of these bonds in the second half of the fiscal.”

Liquidity support

Radhika

Rao, Economist, DBS Group Research, believes that the liquidity support for

bond markets — Centre as well as State bonds – will be timely, helping to keep

a lid on risk-free yields and, by extension, borrowing costs.