The

EU Carbon Border Adjustment Mechanism: New Green Trade Restrictions to Impact

Businesses in India

The EU Carbon Border

Adjustment Mechanism imposes a fee on the carbon emissions contained in certain

imports. We discuss the roll-out of this new mechanism, implications for

India-based manufacturing entities and exporters, and suggest business actions

to prepare for the implementation of the carbon border tax.

On April 18, 2023, the

European Parliament passed legislation for the implementation of a Carbon

Border Adjustment Mechanism (CBAM) as part of the European Union’s (EU) Green

Deal, aimed at reducing greenhouse gas emissions by 55 percent before 2030.

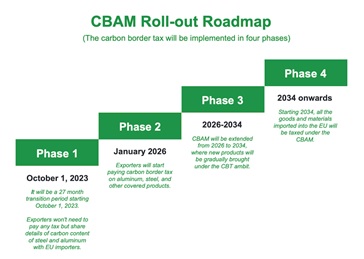

CBAM will be rolled out in four phases and will enable the EU to impose a

Carbon Border Tax (CBT) on specific imports, such as steel, aluminum,

fertilizer, electricity, cement, and hydrogen, from January 2026.

However, CBAM has been

criticized as a trade-restrictive policy, especially by developing countries

like India, which has set a target of becoming carbon neutral by 2070. India

has expressed concerns about CBAM at various international forums, including

the World Trade Organization (WTO), emphasizing the importance of

non-discriminatory treatment for the same products and warning that such

measures could lead to protectionist practices.

What is the EU

carbon border adjustment mechanism and how will it function?

CBAM, or the Carbon

Border Adjustment Mechanism, is designed to ensure fair competition by addressing

the cost of carbon paid by EU installations that follow the EU Emissions Trading

System (ETS), and imported products. It works by applying a fee on the carbon emissions

in certain imports that is equal to the fee imposed on domestic products under the

ETS. By doing so, CBAM helps prevent carbon leakage, where companies relocate their

manufacturing operations outside the EU to avoid the expenses of adhering to climate

regulations.

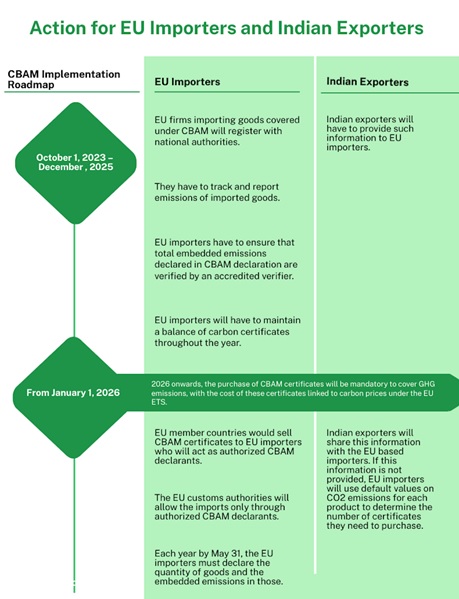

From October 1,

2023, until December 31, 2025, the transitional phase of CBAM will only require

quarterly reports on the greenhouse gas emissions of specific products imported

into the EU, covering both direct and indirect emissions. However, from 2026 onwards,

the purchase of CBAM certificates will be mandatory to cover GHG emissions, with

the cost of these certificates linked to carbon prices under the EU ETS. CBAM will

result in an additional cost for exporting to the EU market, which will be shared

between the exporter or producer and could impact their marketing strategies. It

is expected that other countries may also adopt policies similar to CBAM.

Riccardo Benussi, Head of European Business Development at Dezan

Shira & Associates, notes: “Despite its green intentions, the newly passed CBAM

regulation in the EU Parliament is drawing criticism from countries like China,

India, some US industries, and many industries in developing countries because many

manufacturers in these countries still rely heavily on coal-fired electricity. As

the first carbon import tax law in the world, the regulation means that companies

exporting iron, steel, fertilizers, or cement to EU businesses will have to calculate

and pay for the greenhouse and carbon emissions associated with each product. If

the added cost cannot be absorbed, companies would then have to explore trading

with countries that do not have such a tax or revise their production methods to

emit less greenhouse gases or carbon. While this may be good for the environment,

it could contribute to supply chain fragmentation and increased costs. Therefore,

businesses should carefully assess the potential impact of CBAM on their operations

and explore ways to become more environmentally sustainable in the long term to

avoid potential disruptions to their business activities.”

What products and sectors fall under the scope of

CBAM?

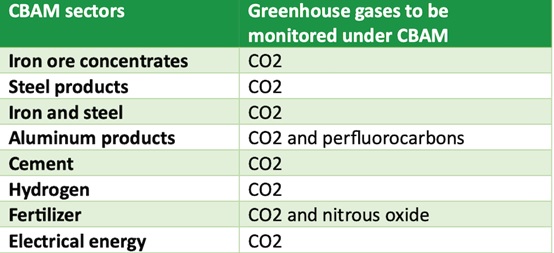

CBAM will initially

apply to particular products within the most carbon-intensive industries, such as

iron and steel, cement, fertilizers, aluminum, electricity,

and hydrogen. It will also include some precursors and a limited number of downstream

products. For cement and fertilizers, only indirect emissions will be considered.

However, the CBAM Regulation requires the European Commission to establish

a timeline to gradually integrate all products covered under the EU ETS, including

indirect emissions, as well as emissions from international transportation, by 2030.

Impact of CBAM on Indian exports to the EU market

and mitigation strategies

The implementation

of the CBAM by the EU is expected to have a significant economic impact on India’s

exports of energy-intensive products such as steel, aluminum,

cement, and fertilizers. Indian exporters are likely to face higher prices, reduced

competitiveness, and lower demand for their goods in the EU market.

The steel industry

is considered a hard-to-abate sector and is responsible for almost eight percent

of global emissions. The International Energy Agency (IEA) reports that carbon emissions

from the iron and steel sector have increased over the past decade, mainly due to

the rise in steel demand and the energy required for its production.

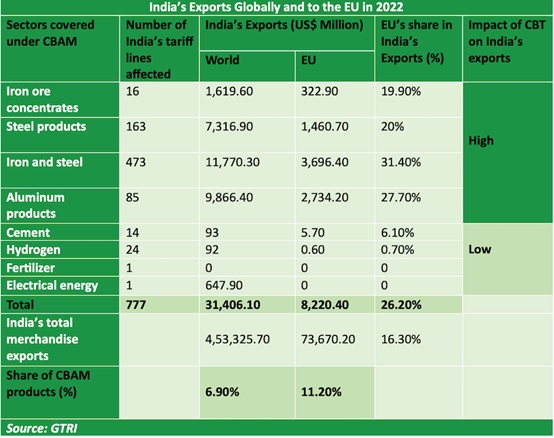

According to a

recent report by the Global Trade Research Initiative (GTRI), the implementation

of the CBAM is expected to pose a significant challenge to India’s metal sector.

In 2022, 27 percent of India’s exports of iron, steel, and aluminum

products worth US$8.2 billion went to the EU. Starting January 1, 2026, the EU will

begin collecting carbon tax on each consignment of steel and aluminum, which will result in Indian firms paying an amount

equivalent to 20-35 percent of tariffs.

Ultimately, the

impact of CBAM on India will depend on the carbon intensity of the exported products

and their substitutes in the EU market. Products with high carbon intensity are

likely to face higher charges, making them less competitive. However, if there are

no low-carbon substitutes for Indian products in the EU market, then the impact

of CBAM on Indian exports may be limited.

One of the major

challenges for India is its lack of an emissions trading system like the EU’s ETS.

Without an ETS, it could be difficult for Indian businesses to demonstrate that

their products are produced using low-carbon technology, resulting in higher CBAM

charges.

To remain competitive

in the global market and mitigate the impact of CBAM, India needs to implement a

carbon pricing mechanism and develop low-carbon technologies. This will help Indian

businesses to comply with the CBAM regulations and reduce the carbon intensity of

their products. Additionally, India needs to review its export strategy and identify

alternative markets where its products can be competitive despite the impact of

CBAM in the EU market.

Impact of CBAM on manufacturing in India and mitigation

strategies

Smart manufacturing

is the use of advanced technologies, such as the Internet of Things (IoT), Artificial

Intelligence (AI), and Big Data Analytics, to optimize manufacturing processes.

It enables companies to reduce costs, improve quality, and increase efficiency.

India’s manufacturing

industry is expected to be significantly affected by the EU’s new carbon border

tax, especially companies that export products to the EU. The policy may affect

the competitiveness of Indian manufacturers, as they may need to pay higher taxes

on their products compared to their EU counterparts. This could lead to a shift

in demand towards EU-made products, affecting the Indian manufacturing industry.

The Indian government

is taking proactive steps to ensure the country’s manufacturing industry remains

competitive by reducing carbon emissions

Indian companies

can adopt several strategies to mitigate the impact of the CBAM on smart manufacturing.

One approach is to invest in renewable energy sources and energy-efficient technologies

to reduce carbon emissions. This will help reduce the amount of tax they need to

pay under the CBAM. Another strategy is to optimize supply chain processes to reduce

the carbon footprint of their products.

Companies can also

diversify their export markets to reduce their dependence on the EU and engage with

policymakers to influence the design and implementation of the CBAM.

Key actions for Indian businesses to prepare for CBAM implementation

·

Indian businesses should assess the potential impact of CBAM on their operations

by examining customs data, purchase data, bill of material, transactional model,

and logistic flows to determine CBAM applicability.

·

To evaluate the potential costs of CBAM, businesses should quantify their

exposure by calculating the potential impact of CBAM costs and expected costs for

administrative governance. They should then analyze the

impact on supply chain and procurement strategies to inform future strategic analysis.

·

Indian businesses must analyze data availability

and quality to ensure they have the necessary data to comply with CBAM requirements.

They should determine which data elements are needed, assess data quality, and close

any respective gaps to prepare for expected administrative obligations.

·

Businesses must review their global value chain and footprint as they relate

to the EU region and CBAM. They should also consider EU ETS implications to determine

cost optimization options and better understand the strategy for investing in manufacturing

installations to reduce emissions and transform to alternative products.

·

Businesses should analyze the impact of CBAM on

their business model and identify opportunities for strategic transformation to

reduce its impact, particularly in terms of their competitiveness in the EU market

and corporate value.

Actionable measures for Indian government to minimize the impact of CBT

India has voiced

its apprehensions regarding the EU Carbon Border Adjustment Mechanism and asserted

that it may act as a trade impediment and could breach WTO regulations. Nevertheless,

India is also committed to reducing its carbon emissions with a goal to achieve net-zero emissions by 2070.

In March 2022,

India’s Commerce and Industry Minister, Piyush Goyal, held talks with his EU counterpart,

Valdis Dombrovskis, to address India’s concerns regarding the implementation of

CBAM. The EU had expressed its willingness to collaborate with India on the issue,

and during the meeting, Goyal had urged the EU to consider alternative solutions

that would not negatively impact Indian industries.

India is currently

in the process of establishing a carbon market, and it is anticipated that the Bureau

of Energy Efficiency (BEE) will announce a Carbon Credits Trading Scheme (CCTS)

by mid-year. The Ministry of Power released a CCTS draft on March 27, which outlines

the institutional framework and operational mechanism for the Indian carbon credit

market.

Meanwhile, the

Indian government is also considering several measures to address the potential

impact of the EU’s carbon border tax:

·

Negotiating with the EU: India’s government plans to engage in discussions with the EU to negotiate

an exemption or a reduced rate for Indian manufacturers. The goal is to ensure that

Indian companies are not unfairly penalized for their emissions.

·

Developing a carbon pricing mechanism: India’s government is also considering the development

of a domestic carbon pricing mechanism to encourage companies to reduce their emissions.

This would help to align India’s policies with the EU’s carbon reduction goals and

make Indian businesses more competitive.

·

Promoting renewable energy: India’s government is already working to promote renewable energy sources,

such as solar and wind power, to reduce carbon emissions. The government plans to

continue to invest in renewable energy infrastructure to help Indian manufacturers

transition to cleaner energy sources.

·

Investing in carbon capture technology: India’s government is also exploring the potential

of carbon capture and storage (CCS) technology to reduce carbon emissions from manufacturing

processes. This technology captures carbon emissions before they are released into

the atmosphere and stores them underground.