WTO Expects Trade Upturn in

2014, 2015

World trade is

expected to grow by a modest 4.7% in 2014 and at a slightly faster rate of 5.3%

in 2015 WTO economists said on 14 April.

Although the 2014 forecast

of 4.7% is more than double the 2.1% increase of last year, it remains below

the 20-year average of 5.3%. For the past two years, growth has averaged only

2.2%.

The sluggish pace of

trade growth in 2013 was due to a combination of flat import demand in

developed economies (-0.2%) and moderate import growth in developing economies

(4.4%). On the export side, both developed and developing economies only

managed to record small, positive increases (1.5% for developed economies, 3.3%

for developing economies).

·

The trade forecast for 2014

has been

upgraded to 4.7% from

4.5%, still

below the 20-year average of 5.3% (1983–2013). A 5.3% increase in trade is anticipated for 2015.

·

Risks to the forecast have

eased in

developed economies but risen in developing countries, as the end of quantitative easing has increased financial market volatility.

·

World merchandise trade

grew 2.1% in 2013 in volume terms,

very close to the 2.3% increase from the previous year.

·

Developing economies trade

flows

turned negative in the middle of 2013, as exports and imports each fell 1% between the first half and the second. Developed economies staged a modest recovery, as exports and imports rose 1% and 1.5%, respectively, during the same period.

“Concluding the Doha

round would provide a strong foundation for trade in the future, and a powerful

stimulus in today’s slow growth environment. We are currently discussing new

ideas and new approaches which would help us to get the job done – and to do it

quickly.”

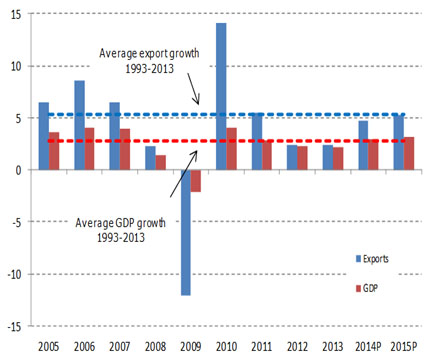

Chart 1: Growth in volume

of world merchandise exports and GDP, 2005-15 a (Annual % change)

a Figures for 2013 and 2014 are projections.

Source: WTO Secretariat.

Several factors

contributed to the weakness of trade and output in 2013, including the lingering

impact of the EU recession, high unemployment in euro area economies (Germany

being a notable exception), and uncertainty about the timing of the Federal

Reserve’s winding down of its monetary stimulus in the United States. The

latter contributed to financial volatility in developing economies in the

second half of 2013, particularly in certain “emerging” economies with large

current account imbalances.

The preliminary

estimate of 2.1% for world trade growth in 2013 refers to the average of merchandise

exports and imports in volume terms, i.e. adjusted to account for differences

in inflation and exchange rates across countries. This figure is slightly lower

than the WTO’s most recent forecast of 2.5% for 2013, issued last September.

The main reason for the divergence was a stronger than expected decline in

developing economies’ trade flows in the second half of last year. For the

second consecutive year, world trade has grown at roughly the same rate as

world GDP (gross domestic product, a measure of countries’ economic output) at

market exchange rates, rather than twice as fast, as is normally the case

(Chart 1).

Recent business

surveys and industrial production data point to a firming up of the recovery in

the United States and Europe in early 2014. The gradual improvement of US

employment data has allowed the Federal Reserve to proceed with its planned

“tapering”, of their third round of quantitative easing (“QE3”) The outlook for

the European Union has also improved, although growth there will remain uneven

as long as peripheral EU economies continue to underperform core ones. Output

growth in Japan should be slightly lower this year as planned fiscal

consolidation

is implemented.

Finally, despite having hit a soft patch recently, developing economies

(including China) should continue to outpace developed economies in terms of

GDP and trade growth in the coming year, but some could encounter setbacks,

particularly those most exposed to the recalibration of monetary policy in

developed countries.

In 2013, the dollar

value of world merchandise exports rose 2.1% to $18.8 trillion. This growth

rate was slightly less than the WTO’s export volume growth estimate for the

year (+2.4%), which implies that export prices declined slightly from one year

to the next. Meanwhile, the value of world commercial services exports rose

5.5% to $4.6 trillion.

The trade forecast

for 2014 is premised on an assumption of 3.0% growth in world GDP growth at

market exchange rates, while the forecast for 2015 assumes output growth of

3.1%. Note that the GDP figures are consensus estimates and are not WTO

projections. Risks to the trade forecast are still mostly on the downside, but

there is some upside potential, particularly since trade in developed economies

is starting from a low base. However, volatility is likely to be a defining

feature of 2014 as monetary policy in developed economies becomes less

accommodative.

Some developed

economy risks factors have receded considerably since last year’s press

release, including the sovereign debt crisis in Europe and fiscal brinksmanship

between the executive and legislative branches of government in the United

States. Developing economies are now the focus of several gathering risks,

including large current account deficits (e.g. India, Turkey), currency crises

(Argentina), overinvestment in productive capacity, and rebalancing economies

to rely more on domestic consumption and less on external demand.

Geopolitical risks

have introduced an additional element of uncertainty to the forecast. Civil

conflicts and territorial disputes in the Middle East, Asia and Eastern Europe

could provoke higher energy prices and disrupt trade flows if they escalate.

However, since the timing and impact of these kinds of risks are inherently

unpredictable, they are not considered directly in our forecasts.

More details on

trade developments in 2013

The WTO and UNCTAD

jointly produce a variety of short-term trade statistics, including

seasonally-adjusted quarterly merchandise trade volume indices. These are shown

in Chart 2 for the United States, the European Union, Japan and developing Asia

(which includes China).

After a flat first

quarter, US exports grew steadily for the remainder of 2013. In contrast,

exports from the Europe Union to the rest of the world (i.e. extra-EU exports)

were strongest in the first quarter but weakened and turned negative over the

course of the year. Trade between EU countries (i.e. intra-EU exports) rallied

slightly in the third quarter but stalled in other periods. Japan saw its

exports increase in three out of four quarters in 2013, starting from a low

base. Finally, exports from developing Asia treaded water, alternating between

positive and negative but trending flat.

Overall, exports in

the second half of the year were up for the United States (3.3%), intra-EU

(2.0%), and Japan (1.2%), while developing Asia was flat (0.0%) and extra-EU

slightly negative (-1.5%).

On the import side,

extra-EU trade trended down throughout the year, sapping global demand. (The

story for intra-EU imports is the same as for intra-EU exports, see above.)

Meanwhile, US and Japanese imports were generally rising, and developing Asia

was mostly flat, only turning negative in the fourth quarter.

In the second half,

import demand was improving in some large markets (+2.2% for the US, +1.8% for

intra-EU, +0.2% for extra-EU, and +3.3% for Japan), and was slightly negative

in developing Asia (-0.2%). However, exporters will find little relief until EU

imports recover substantially from their current depressed state. (EU

merchandise imports represent 32% of world imports including intra-EU trade,

and 15% of world imports excluding it.)

Chart 2: Quarterly merchandise trade flows of selected

economies, 2010Q1-2013Q4

Seasonally adjusted volume indices, 2010Q1=100Source

Although

not shown in Chart 2, quarterly exports and imports of developing economies in

total turned negative in the second half of last year, with exports and imports

each falling around 2% between the second and fourth quarters. South and

Central America’s

trade flows were particularly affected (the region’s exports declined by 3% and

its imports contracted by 5% during the same period) but other natural resource

exporting regions were hit hard as well. However, the declines in developing

regions were roughly cancelled by the rising trend for developed economies.

For

the second time in two years, merchandise trade has grown more slowly than one

would expect given the growth of the world economy as measured by GDP. Although

trade can grow faster or more slowly than output in any given year, since the

1990s it has tended to grow about twice as fast as GDP when measured at market

exchange rates. In 2012 trade growth fell to the same rate as GDP, and they

remained at matching rates in 2013, prompting analysts to question whether the

previous relationship continued to hold.

Chart

3 shows 10-year moving averages of world trade growth, world GDP growth and

their ratio. This ratio peaked at 2.4 in 2000 but has since fallen to 1.7 in

2013. Historically, trade has tended to contract when world output has slowed,

only to rebound sharply afterwards. Structural factors (e.g. the spread of

supply chains, the product composition of world trade, subtle protectionism,

etc.) may have played a role in the declining ratio. However, given the number

and severity of global slowdowns in recent years, the explanation may simply be

cyclical. It is too soon to say whether something like a 2:1 relationship

between trade growth and GDP growth will reassert itself once the global

recovery gains traction, but this variable will bear watching in the future.

Chart 3: 10-year moving

average of world trade, GDP and trade/GDP, 1990-2015

Average

annual % change (left) and ratio (right)

a Figures for 2014 and 2015 are projections.

Source: WTO Secretariat

Additional perspective on the trade

forecast

The

WTO’s forecast of 4.7% growth in world merchandise trade for 2014 is below the

average rate of 5.3% for the last 20 years (1993–2013) and also below the pre-crisis average rate of

6.0% for 1990–2008

(Chart 4). In addition to creating a permanent shift downward in the level of

trade, the global recession of 2008-09 may have reduced its average growth rate

as well. The average rate of trade expansion in the three years since 2010 is

3.42%. Forecasts for 2014 and 2015, if correct, would raise the average to 4%,

but this rate is insufficient to narrow the existing gap.

Chart 4: Volume of world

merchandise exports, 1990-2015a

Indices,

1990=100

a Figures for 2014 and 2015 are projections.

Source: WTO Secretariat

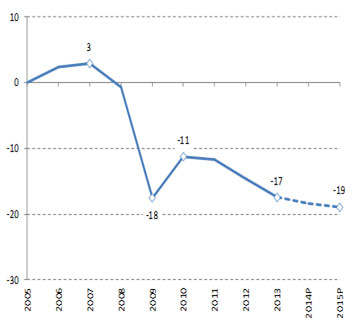

The

divergence between the pre-crisis trend and current levels of world trade continues

to widen. This gap stood at 17.0% of the trend level in 2013 and will rise to

19% by 2014 if our projections are realized, which would place world trade

further below its the pre-crisis trend than it was in 2009 during what

economists have called the “great

trade collapse”

(Chart 5).

In

2012 the EU recession had a significant dampening effect on measured trade

volumes due to the large share of the European Union in world trade (around 1/3

for both exports and imports) and to the fact that, by convention, trade

between EU countries is counted in world trade totals. In last year’s press release, we estimated that

growth in world trade would have been more than a percentage point higher if

the EU was treated as a single entity and intra-EU trade was ignored. A similar

calculation for 2013 did not result in a substantially higher growth rate (2.7%

for world trade excluding intra-EU trade, compared to 2.1% including it)

because although trade within the EU remained depressed it was not declining as

sharply as last year. However, if EU economies recover faster than expected and

trade between them is revitalized, this could cause world trade to surprise on

the upside.

Chart 5: Deviation of

world merchandise export volumes from pre-crisis trends, 2005-15a

percent

a Figures for 2014 and 2015

are projections.

Source: WTO Secretariat

The state of the world

economy and trade in 2013 and 2014Q1

Economic growth

Output trends in developed

economies were decidedly mixed during 2013. The 2012 recession in the European

Union, which was particularly acute in the euro area, extended into 2013 with a

0.2% contraction in EU GDP the first quarter (annualized rate) according to

data from OECD Quarterly National Accounts. Growth remained positive but tepid

for the rest of the year, ranging between 1.2% and 1.7% annualized.

In

contrast to this performance, the United States saw annualized quarterly growth

reach 4.1% in the third quarter, and roughly 2.5% in both Q2 and Q4. After some

delay, the US Federal Reserve announced in December of last year that it would

begin to wind down its QE3 (third quantitative easing) programme of bond

purchases beginning in January. Initial market reaction was muted but

after-shocks were felt soon enough, mostly in developing economies.

Japan’s experiment with expanded fiscal and

monetary stimulus known as Abenomics” produced stronger growth in the first

two quarters of 2013, but activity slowed in the second half of the year,

falling to less than 1% per quarter, annualized.

For

developed economies taken together, GDP growth for the whole of 2013 was 1.1%,

lower than the 1.3% rate recorded in 2012 and 1.5% expansion of 2011 (Table 1).

Developing

economies’

output slowed in 2013 as financial volatility hit some countries harder than

others. Developing economies including the Commonwealth of Independent States

(CIS) saw their collective GDP growth drop to 4.4% from 4.5% in 2012, down from

5.7% in 2011 (Table 1).

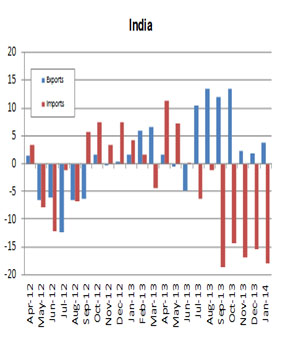

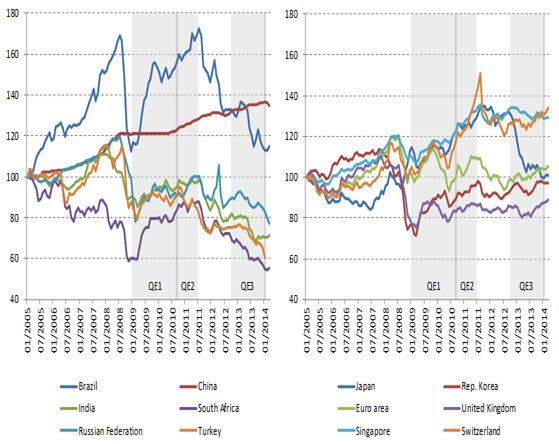

The

rise in financial market volatility was most keenly felt in emerging markets

with large current account deficits. This is especially true of India, where

output growth see-sawed from 2.6% in the second quarter to 7.2% in the third,

then back to 3.9% in the fourth (all rates annualized, sourced from the OECD).

With financial markets anticipating an early tapering of QE3 in mid-2013,

capital flows put pressure on emerging market currencies like India’s Rupee, which suffered a depreciation

of 14.5% between April and September (Chart 6). Other emerging market

currencies also depreciated significantly against the dollar, including the

Argentinean peso, the Turkish lira, the Indonesian rupiah and the South African

rand. Idiosyncratic political shocks contributed further to market turbulence

in Turkey and Thailand.

In

a potentially significant development, China has given its currency greater

leeway to fluctuate against other currencies, and monetary authorities allowed

the RMB to depreciate by 1.5% against the dollar between January and March.

What this portends for the future conduct of Chinese monetary policy remains to

be seen, but Chinese authorities have indicated a desire to gradually move

their currency toward greater convertibility.

Chart 6: US dollar

exchange rates against currencies of selected countries, January 2005 - March

2014

Indices

of US dollars per unit of national currency, 1 January 2005 = 100

Source: Federal Reserve Bank

of St. Louis except for Russian Federation and Turkey, which are sourced from

IMF International Financial Statistics.

Asia

recorded the fastest GDP growth among WTO geographic regions in 2013 at 4.2%,

which was almost equal to growth in the previous two years. It was followed by

Africa (3.8%), Middle East (3.0%), South and Central America (also 3.0%), the

Commonwealth of Independent States (2.0%), North America (1.8%) and Europe

(0.3%).

Table 1: GDP and

merchandise trade by region, 2011-13

Annual

% change

a Includes

the Caribbean

b Hong Kong, China; Republic of Korea; Singapore and Chinese Taipei

Source: WTO Secretariat.

Merchandise trade in volume (i.e.

real) terms

World

merchandise trade volume as measured by the average of exports and imports rose

2.1% in 2013, but the difference between measured exports and imports was

relatively large (2.4% for exports, 1.8% for imports). Some degree of

divergence between these figures is normal due to imperfect data recording and

may be narrowed by future revisions.

Exports

of developed economies grew more slowly than the world average at 1.5%, while

shipments from developing countries grew faster than average at 3.3%. On the

import side, developed economies recorded a small decline of -0.2%, while

developing economies and CIS increased by 4.4% (Table 1).

Asia’s exports grew faster than any other

region’s last year, with a 4.6% rise. It was followed by North America (2.8%),

Europe (1.5%), the Middle East (also 1.5%), South and Central America (0.7%),

the Commonwealth of Independent States (also 0.7%) and Africa (-3.4%). Asia’s

export growth was held back by Japan, which saw is shipments to the rest of the

world decline by 1.8%. Meanwhile, exports of China and India increased by 7.7%

and 6.7%, respectively. These performances were better than 2012 but still

relatively weak by recent historical standards. The negative figure for Africa

was due to sharp reductions in shipments from petroleum exporting countries,

including Libya (-27%), Nigeria (11%) and Algeria (-7%).

Turning

to imports, the fastest growing region was Asia (4.4%), followed by the Middle

East (4.4%), Africa (4.0%), South and Central America (2.5%), North America

(1.2%), Europe (-0.5%), and the Commonwealth of Independent States (-1.1).

India suffered a sharp drop of 2.9% in its imports as a result of its economic

slowdown, but China’s

purchases from abroad jumped nearly 10%.

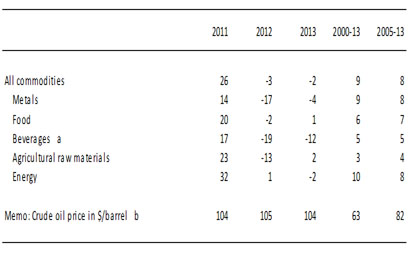

Africa

was able to increase its imports even as its exports fell in 2013 due to

continued high primary commodity prices. Although prices for metals, raw

materials, and beverages (including coffee, tea and cocoa) have fallen in the

last 2 years, oil prices have been remarkably steady, rising 1% in 2012 and

falling 2% in 2013. Primary commodity prices in general only fell 2% last year

(Table 2).

Table 2: World prices of

selected primary products, 2000-13

Annual

% change and $/Barrel

a Comprising coffee, cocoa

beans and tea.

b Average of Brent, Dubai, and West

Texas Intermediate.

Source: IMF

International Financial Statistics.

Merchandise and commercial services

trade in value (i.e. dollar) terms

The

dollar value of world merchandise exports in 2013 was $18.8 trillion, 2% higher

than in 2012. The growth of world merchandise exports in current dollar terms

was nearly equal to the growth of exports in volume terms since prices of

traded goods as measured by unit values were nearly unchanged from one year to

the next. The average growth rate of export values in the post-2005 period

remained stable at 8% (Table 3). One much remarked upon development in 2013 was

the fact that China became the largest trader as measured by the sum of exports

and imports (11.0% of world), overtaking the United States (10.4%). However, if

the EU is treated as a single entity its share in world exports plus imports

excluding intra-EU trade remains the largest, 15.1% compared to China's 13.8%.

Meanwhile,

world commercial services exports in 2013 reached $4.6 trillion, with a growth

rate of 6%. The 2013 growth rate for transport services was below world

commercial services exports at 2%, while travel services grew at 7% and other

commercial services grew at 6% (Table 3).

Commercial

services accounted for 20% of total world trade in world goods and commercial

services in 2013, up 1% from the 2012 share. It should be noted that

traditional trade statistics, which measure gross trade flows rather than value

added at various stages of production, may strongly underestimate the

contribution of services to international trade.

In

dollar terms, China’s

exports of financial services rose 52% to $3 billion in 2013, although the

United States remained the top supplier with exports valued at $82 billion.

Other notable changes include China’s

displacing of France to become the fourth largest exporter of other business

services.

Table 3: World exports of

merchandise and commercial services, 2005-13

$bn and annual % change

Source: WTO Secretariat

estimates for merchandise and WTO and UNCTAD Secretariat estimates for

commercial services.

Some sub-categories of other commercial services grew faster than others. Insurance services and computer and information services recorded the strongest growth at 8%, while construction posted the only decline at -3%. Financial services (i.e. services provided by banks and other financial intermediaries) posted the strongest recovery from a decline of -3% in 2012 to growth of 7% in 2013. Communications services (including postal, courier and telecommunications services) grew at a modest 2% rate and other business services (including engineering services, legal/accounting services, management consulting, advertising and trade related services among others) grew 7%. Royalties and licence fees increased by 6% after stagnating in 2012. However, all sub-categories of other commercial services recorded lower-than-trend growth rates.

Appendix

tables 1 to 6 more provide detailed information on nominal merchandise and

commercial services trade flows by region and for selected economies. They also

include tables of leading exporters and importers with and without trade

between EU states. There were few significant moves up or down in world

rankings last year.

China

overtook Germany as the second largest importer of commercial services compared

to last year’s tables, while France moved into fourth position pushing the

United Kingdom to fifth place.

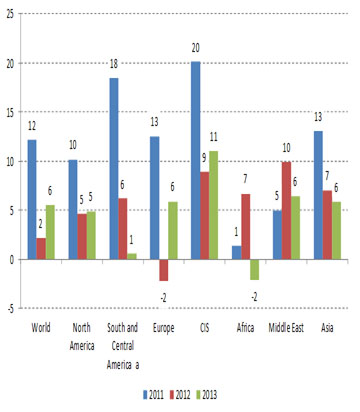

Year-on-year

growth in commercial services exports by region for 2011-13 are shown in Chart

7, below, and in Appendix Table 2. Imports are not shown in the chart, but

their appearance is similar, with sharp declines between 2011 and 2012 for most

regions, followed by smaller changes (some positive, some negative) between 2012

and 2013. On both the export and import sides, growth in European services

trade turned sharply negative in 2012 before rebounding into positive territory

in 2013.

The

strongest decelerations were recorded by South and Central America, for both

exports and imports, with Brazil responsible for much of the decline. On the

export side, growth fell from 18% in 2011 to 6% in 2012, to 1% in 2013. On the

import side it dropped from 23% in 2011 to 7% in 2012 to 6% in 2013.

Chart

7: Growth in the value of commercial services exports by region, 2011 — 13

Annual

% change

a Includes the Caribbean

Source: WTO

Secretariat.

Merchandise trade details

North

America’s merchandise exports rose 1.9% in 2013 to $2.42 trillion (12.9% of

world exports) while imports remained essentially unchanged at $3.20 trillion

(16.9% of world imports). South and Central America’s exports fell by 1.8% to $737 billion

(3.9%) but the region’s

imports grew by 2.4% to $773 billion (4.1%). European exports rose 4.0% to

$6.64 trillion (35.3%), the strongest growth of any region. Meanwhile, Europe’s imports recorded a small increase of

1.0% to $6.59 trillion (34.9%).

Exports

of the Commonwealth of Independent States declined 2.8% to $778 billion while

imports grew by 0.7% to $575 billion. Respectively, the region’s exports and imports represented 4.1

and 3.0% of world trade.

Africa’s exports suffered a large decline of

6.3% to $599 billion (3.2% of world exports). Meanwhile imports grew a modest

2.2% to $628 billion (3.3% of world imports). Middle East exports declined by

1.3% to $1.33 trillion (or 7.1%) and the region’s imports rose by 4.3% to $770 billion (4.1%).

Finally,

Asia’s exports grew by 2.8% to $6.29

trillion (33.5% of the global total) in 2013. Meanwhile, imports grew by 2.1%

to $6.37 trillion (33.6%).

The

top five merchandise exporters in 2013 were China ($2.21 trillion, 11.8% of

world exports), the United States ($1.58 trillion, 8.4%), Germany ($1.45

trillion, 7.7%), Japan ($715 billion, 3.8%) and the Netherlands ($664 billion,

3.5%). There were no changes in rank among the top exporters, although Japan

suffered a sharp decline of 10.5% in exports.

The

leading importers were the United States ($2.33 trillion, 12.4% of world

imports), China ($1.95 trillion, 10.3%), Germany ($1.19 trillion, 6.3%), Japan

($833 billion, 4.4%) and France ($681 billion, 3.6%). France replaces the

United Kingdom at number five on the list of leading importers.

If

we count all 28 European Union members as a single entity and exclude intra-EU

trade, the leading exporters were the European Union ($2.30 trillion, or 15.3%

of world exports), China (14.7%), the United States (10.5%), Japan (4.8%) and

the Republic of Korea ($560 billion, 3.7%). The leading importers when intra-EU

trade is excluded were the United States (15.4% of world imports), the European

Union ($2.23 trillion, 14.8%), China (12.9%), Japan (5.5%), and Hong Kong,

China ($622 billion, 4.1%).

Merchandise trade developments by

manufacturing sector

Chart

8 shows estimated year-on-year growth in the dollar value world trade for

selected categories of manufactured goods. Growth turned negative for most

products, except for office and telecom equipment, at the beginning of 2012,

and remained negative until mid-2013. By 2013Q2 most categories had returned to

positive (albeit slow) year-on-year growth, but even as late as Q4 iron and steel

remained below its level of one year earlier.

Iron

and steel trade is a very pro-cyclical and somewhat lagging indicator of

economic activity. At the beginning of 2013 world trade in iron and steel was

down 10% compared to a year earlier, but by the end of the year it was still

down 4%.

Automotive

products trade is equally cyclical but leading. In the first quarter of 2013

trade in vehicles and parts had dropped 4% from its level a year earlier, but

by Q4 trade in automotive products was 9% higher than a year earlier. This

rebound bodes well for the economic recovery and for trade in inputs to

automobile production, including iron and steel, electronics and various raw

materials.

Chart 8: Quarterly world

exports of manufactured goods by product, 2008Q1-2013Q4

Year-on-year

% change in US dollar values

Source: WTO Secretariat

estimates based on mirror data for available reporters in the Global Trade

Atlas database, Global trade Information Systems.

Prospects for 2014 and 2015

Prospects

for world trade and output in 2014 and 2015 are better than they have been for

some time, but leading economies remain fragile, including some of the most

dynamic developing countries that until recently were propping up global

demand. Downside risks to trade abound, but significant upside potential also

exists, as the US economy seems to be gaining momentum and the European Union

appears to have turned a corner. At the same time, developing economies have

slowed appreciably, for a variety of reasons both internal and external. Which

of these forces is stronger may determine how world trade evolves over the next

1 to 2 years.

In

order to provide a more complete picture of the trade outlook, the WTO has

produced more detailed forecasts this year, including breakdowns by geographic

region and by level of development (Table 4). Forecasts for North America,

South and Central America, Europe and Asia are shown separately, whereas data

for Africa, the Middle East and the CIS are aggregated together due to their

economic similarity as petroleum exporting regions, and also because statistics

for these regions rely more on estimation due to incomplete data.

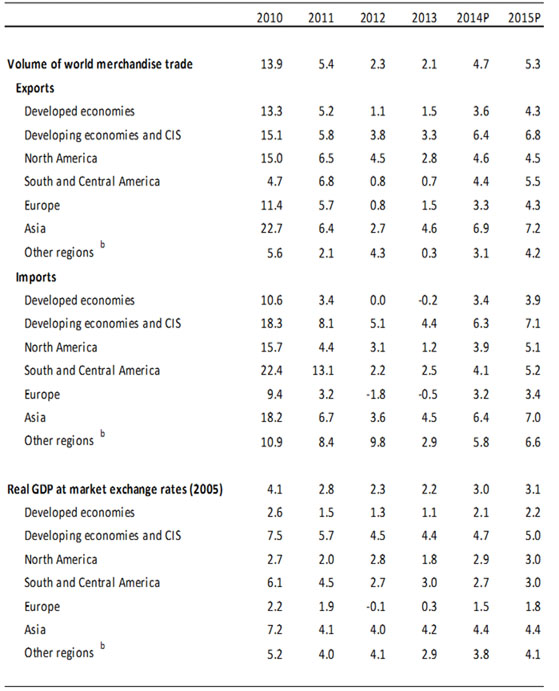

World

merchandise trade is expected to post a 4.7% increase in 2014, with developed

economies growing 3.6% and developing economies and the CIS advancing 6.4%. We

expect that exports from Asia will grow faster than those from any other region

(6.9%). Asia should be followed by North America (4.6%), South and Central

America (4.4%), Europe (3.3%), and Other regions (3.1%), an aggregate that

includes Africa, CIS and Middle East. Exports will be supported by rising

import demand on the part of developed countries as the US economy gains

momentum, and by improving economic conditions in Europe. However, the extent

of the gains will be limited by the high level of unemployment in European

countries and the still considerable amount of slack in the US labour market

due to low labour force participation.

On

the import side, the 4.7% increase in world trade in 2014 will be split between

developed economies growing at 3.4%, and developing economies growing at 6.3%.

Asia should also lead all regions in import growth in 2014 (6.4%), followed by Other regions (5.8%), South and Central America (4.1%),

North America (3.9%), and finally Europe (3.2%). However, Asian import growth

is likely to be unbalanced, with larger gains in China and smaller increases in

other developing Asian economies.

Two

year forecasts are provisional estimates based on strong assumptions about the

medium-term trajectory of gross domestic product (GDP) and should be

interpreted with care. Merchandise trade is projected to grow by 5.3% in 2015,

with developed and developing economies posting increases of 4.3% and 6.8%,

respectively, on the export side, as well as gains of 3.9% and 7.1% on the

import side. For the year we expect to see Asia’s exports grow faster than in 2014 (7.2%), followed by

those of South and Central America (5.5%), North

America (4.5%), Europe (4.3%), and Other regions (4.2%). In 2015, import growth

of Asia should accelerate to 7.0%. Other regions will have the second fastest

import growth (6.6%) followed by South and Central America (5.2%), North

America (5.1%) and Europe (3.4%).

Trade

growth this year could fall short of estimates if some downside risks emerge,

including financial turbulence in emerging markets related to the conduct of

monetary policy in the United States and other developed countries. Better than

expected growth in the US could actually provoke further instability in

developing economies as it might be interpreted as portending earlier interest

rate rises. This in turn could trigger further capital outflows from the

developing world as investors seek improved returns in developed countries.

However, the prospect of deflation in the euro area suggests that monetary

policy in developed countries could as easily become looser rather than

tighter.

Table 4: World merchandise

trade and GDP, 2010-2015a

Annual

% change

a Figures for 2014 and 2015

are projections.

b Other regions comprises the Africa,

CIS and Middle East

Source: WTO

Secretariat for trade, concensus estimates for GDP.

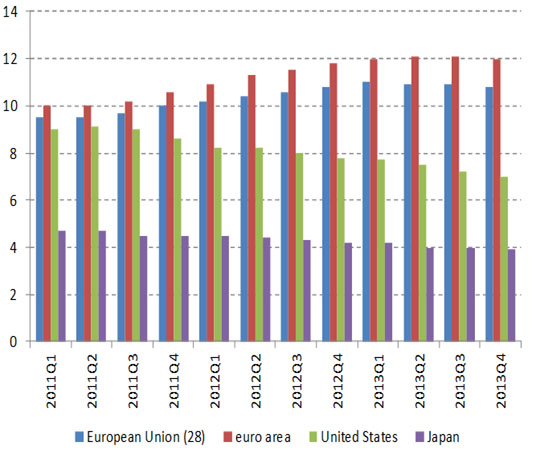

The

high level of joblessness in the euro area could act as a brake on global import

demand for some time to come since unemployment rates tend to decline only

gradually. The recent experience of the United States gives us an indication of

how much time might be required. From its peak at just under 10% in March of

2010, it took 44 months -

more than three and a half years - for the US unemployment rate to fall to 7%

(Chart 9). Until the EU rate comes down, European demand will likely only

provide marginal support for stronger global trade growth.

Chart 9: Unemployment rates in the European Union (28), the

euro area, the United States and Japan, 2010Q1-2013Q4

Annualized % change over previous quarter

Source:

OECD Labour Force Statistics

India Keeps 19th Position in

World Exports but Moves Down to 12th Place in World Imports

China Maintains 1st in Exports with 11.8% World Share

Merchandise Trade: Leading Exporters and Importers,

2013

|

$bn and % |

|||||||||||

|

Rank 2013 |

Rank 2012 |

Exporters |

Value |

Share |

Annual % change |

Rank 2013 |

Rank 2012 |

Importers |

Value |

Share |

Annual % change |

|

1 |

(1) |

China |

2210 |

11.8 |

8 |

1 |

(1) |

United States |

2331 |

12.4 |

0 |

|

2 |

(2) |

United States |

1579 |

8.4 |

2 |

2 |

(2) |

China |

1950 |

10.3 |

7 |

|

3 |

(3) |

Germany |

1453 |

7.7 |

3 |

3 |

(3) |

Germany |

1187 |

6.3 |

2 |

|

4 |

(4) |

Japan |

715 |

3.8 |

-10 |

4 |

(4) |

Japan |

833 |

4.4 |

-6 |

|

5 |

(5) |

Netherlands |

664 |

3.5 |

1 |

5 |

(6) |

France |

681 |

3.6 |

1 |

|

6 |

(6) |

France |

580 |

3.1 |

2 |

6 |

(5) |

United Kingdom |

654 |

3.5 |

-5 |

|

7 |

(7) |

Korea, Republic of |

560 |

3.0 |

2 |

7 |

(8) |

Hong Kong, China |

622 |

3.3 |

12 |

|

|

|

|

|

|

|

|

|

retained imports |

141 |

0.7 |

4 |

|

8 |

(11) |

United Kingdom |

541 |

2.9 |

15 |

8 |

(7) |

Netherlands |

590 |

3.1 |

0 |

|

9 |

(10) |

Hong Kong, China |

536 |

2.9 |

9 |

9 |

(9) |

Korea, Republic of |

516 |

2.7 |

-1 |

|

|

|

domestic exports |

20 |

0.1 |

-11 |

|

|

|

|

|

|

|

|

|

re-exports |

516 |

2.7 |

10 |

|

|

|

|

|

|

|

10 |

(8) |

Russian Federation |

523 |

2.8 |

-1 |

10 |

(11) |

Italy |

477 |

2.5 |

-2 |

|

11 |

(9) |

Italy |

518 |

2.8 |

3 |

11 |

(12) |

Canada a |

474 |

2.5 |

0 |

|

12 |

(13) |

Belgium |

469 |

2.5 |

5 |

12 |

(10) |

India |

466 |

2.5 |

-5 |

|

13 |

(12) |

Canada |

458 |

2.4 |

1 |

13 |

(13) |

Belgium |

450 |

2.4 |

3 |

|

14 |

(14) |

Singapore |

410 |

2.2 |

0 |

14 |

(14) |

Mexico |

391 |

2.1 |

3 |

|

|

|

domestic exports |

219 |

1.2 |

-4 |

|

|

|

|

|

|

|

|

|

re-exports |

191 |

1.0 |

6 |

|

|

|

|

|

|

|

15 |

(16) |

Mexico |

380 |

2.0 |

3 |

15 |

(15) |

Singapore |

373 |

2.0 |

-2 |

|

|

|

|

|

|

|

|

|

retained imports b |

182 |

1.0 |

-9 |

|

16 |

(15) |

Saudi Arabia, Kingdom of c |

376 |

2.0 |

-3 |

16 |

(16) |

Russian Federation a |

344 |

1.8 |

3 |

|

17 |

(18) |

United Arab Emirates c |

365 |

1.9 |

4 |

17 |

(17) |

Spain |

339 |

1.8 |

0 |

|

18 |

(20) |

Spain |

316 |

1.7 |

7 |

18 |

(18) |

Taipei, Chinese |

270 |

1.4 |

0 |

|

19 |

(19) |

India |

312 |

1.7 |

5 |

19 |

(21) |

Turkey |

252 |

1.3 |

6 |

|

20 |

(17) |

Taipei, Chinese |

305 |

1.6 |

1 |

20 |

(20) |

Thailand |

251 |

1.3 |

0 |

|

21 |

(21) |

Australia |

253 |

1.3 |

-1 |

21 |

(22) |

Brazil |

250 |

1.3 |

7 |

|

22 |

(22) |

Brazil |

242 |

1.3 |

0 |

22 |

(23) |

United Arab Emirates c |

245 |

1.3 |

7 |

|

23 |

(25) |

Switzerland |

229 |

1.2 |

1 |

23 |

(19) |

Australia |

242 |

1.3 |

-7 |

|

24 |

(23) |

Thailand |

229 |

1.2 |

0 |

24 |

(25) |

Malaysia |

206 |

1.1 |

5 |

|

25 |

(24) |

Malaysia |

228 |

1.2 |

0 |

25 |

(26) |

Poland |

204 |

1.1 |

2 |

|

26 |

(27) |

Poland |

202 |

1.1 |

9 |

26 |

(24) |

Switzerland |

200 |

1.1 |

1 |

|

27 |

(26) |

Indonesia |

184 |

1.0 |

-3 |

27 |

(27) |

Indonesia |

187 |

1.0 |

-2 |

|

28 |

(29) |

Austria |

174 |

0.9 |

5 |

28 |

(28) |

Austria |

182 |

1.0 |

2 |

|

29 |

(28) |

Sweden |

167 |

0.9 |

-3 |

29 |

(30) |

Saudi Arabia, Kingdom of |

164 |

0.9 |

5 |

|

30 |

|

Czech Republic |

161 |

0.9 |

3 |

30 |

(29) |

Sweden |

158 |

0.8 |

-3 |

|

|

|

Total of above d |

15339 |

81.7 |

- |

|

|

Total of above d |

15492 |

82.1 |

- |

|

|

|

World d |

18784 |

100.0 |

2 |

|

|

World d |

18874 |

100.0 |

1 |

World prices of

selected primary products, 2000-13

Annual % change and $/Barrel

|

|

2011 |

2012 |

2013 |

2000-13 |

2005-13 |

|

All commodities |

26 |

-3 |

-2 |

9 |

8 |

|

Metals |

14 |

-17 |

-4 |

9 |

8 |

|

Food |

20 |

-2 |

1 |

6 |

7 |

|

Beverages a |

17 |

-19 |

-12 |

5 |

5 |

|

Agricultural raw

materials |

23 |

-13 |

2 |

3 |

4 |

|

Energy |

32 |

1 |

-2 |

10 |

8 |

|

Memo: Crude oil

price in $/barrel b |

104 |

105 |

104 |

63 |

82 |

a.

Comprising coffee, cocoa beans and tea

b.

Average of Brent, Dubai and West Texas Intermediate

Source: IMF International Financial

Statistics.