WTO Says World Trade Growth Falls to 2.5%

in 2012

Recovery

in 2013 to only 4.5% Rise

Slowing global output growth has led WTO economists

to downgrade their 2012 forecast for world trade expansion to 2.5% from 3.7% and

to scale back their 2013 estimate to 4.5% from 5.6%.

The global economy has encountered increasingly

strong headwinds since the last WTO Secretariat forecast was issued in April.

Output and employment data in the United States have continued to disappoint,

while purchasing managers’ indices and industrial production figures in China

point to slower growth in the world’s largest exporter.

More importantly, the European sovereign debt

crisis has not abated, making fiscal adjustment in the peripheral euro area

economies more painful and stoking volatility. Figures for world trade include

trade between EU countries (i.e. EU intra-trade), making them highly sensitive

to developments in this region.

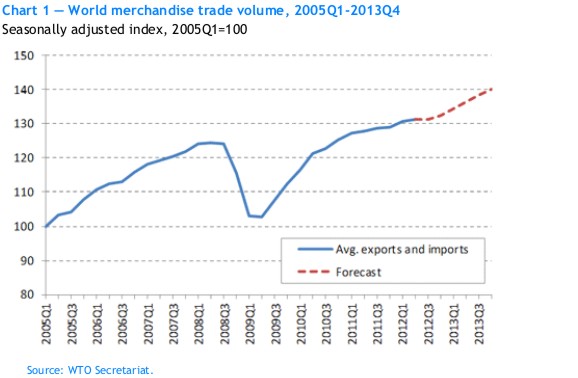

All of these factors have contributed to an easing

of global trade growth, which slowed to a crawl in the second quarter according

to new quarterly merchandise trade volume statistics compiled by the WTO (Chart

1 and box).

The volume of world trade as measured by the

average of exports and imports only managed to grow 0.3% in the second quarter

compared to the first, or 1.2% at an annualized rate.

The trade slowdown in the first half of 2012 was

driven by an even stronger deceleration in imports of developed countries and

by a corresponding weakness in the exports of developing economies, which for

the purposes of this analysis includes the Commonwealth of Independent States.

The WTO now expects world merchandise trade volume

to grow by 2.5% in 2012 (down from 3.7% in April). On the export side, we

anticipate a 1.5% increase in developed economies’ trade (down from 2%) and a

3.5% expansion for developing countries (down from 5.6%). On the import side,

we foresee nearly stagnant growth of 0.4% in developed economies (down sharply

from 1.9%) and a more robust 5.4% increase in developing countries (down from

6.2%).

Table

1: World merchandise trade volume and GDP, 2008-2013a

|

Annual % change |

||||||

|

|

2008 |

2009 |

2010 |

2011 |

2012a |

2013a |

|

Volume of World

Merchandise Tradeb |

2.3 |

-12.5 |

13.9 |

5.0 |

2.5 |

4.5 |

|

Exports |

|

|

|

|

|

|

|

Developed

Economies |

0.9 |

-15.2 |

13.0 |

4.6 |

1.5 |

3.3 |

|

Developing

Economies and CIS |

4.3 |

-7.8 |

15.3 |

5.3 |

3.5 |

5.7 |

|

Imports |

|

|

|

|

|

|

|

Developed

Economies |

-1.1 |

-14.4 |

11.0 |

2.9 |

0.4 |

3.4 |

|

Developing

Economies and CIS |

8.6 |

-10.5 |

18.3 |

8.3 |

5.4 |

6.1 |

|

Real GDP at market

exchange rate |

1.3 |

-2.4 |

3.8 |

2.4 |

2.1 |

2.4 |

|

Developed

Economies |

0.0 |

-3.8 |

2.7 |

1.5 |

1.2 |

1.5 |

|

Developing

Economies and CIS |

5.6 |

2.2 |

7.3 |

5.3 |

4.9 |

5.2 |

a Figures for 2012 and 2013 are

projections.

b Average of exports and imports.

Source:

WTO Secretariat for trade, consensus estimates of economic forecasters for GDP.

Figures for 2013 are provisional estimates based on

strong assumptions about medium-term economic developments, including:

i. that current policy measures will be

sufficient to avert a breakup of the euro, and

ii. an agreement will be

reached to stabilize public finances in the United States, thereby avoiding

automatic spending cuts and tax increases early next year.

Failure of these and other assumptions could derail

the latest projections.

As a result, these figures should be interpreted

with caution. Based on current information, the WTO expects trade growth to

rebound to 4.5% in 2013. Exports of developed and developing economies should

increase by 3.3% and 5.7%, respectively, while imports of developed and

developing countries should advance 3.4% and 6.1%.

Although developed countries collectively recorded

modest increases in both exports and importsin2012, some grew faster than

others.

Exports of the United States and shipments from the

EU to the rest of the world (i.e. extra-EU exports) grew steadily over the past

year, with year-on-year increases of around 7% and 5%, respectively, in the

second quarter.

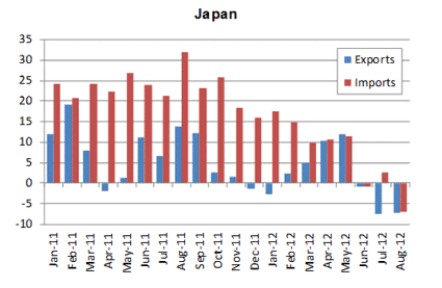

Japanese exports have been mostly flat since

mid-2010, but even they recorded an 8.5% year-on-year increase in the second

quarter. Imports of the United States and Japan have also held up relatively

well despite the crisis, with year-on-year growth of roughly 5% and 6% in the

latest period.

However, import demand in the

European Union has weakened significantly, resulting in less tradebetween EU countries (intra-trade down3.5%

year-on-year in the second quarter) and fewer imports from the rest of the

world (also down 3.5%). The weight of the EU in total world trade (around 35%

on both the export and import sides in 2011, including EU-intra trade),

combined with the larger-than-expected year-on-year drop in EU imports through

the first half of 2012, explains much of the downward revision to the forecast.

The EU also represents nearly 60% of developed economies’ imports, which

accounts for the stagnation in projected imports of developed economies in

2012.

Weak import demand in developed countries and

softer domestic demand in China have contributed to sagging trade flows in the developing

world, most noticeably in dynamic export-oriented economies in Asia.

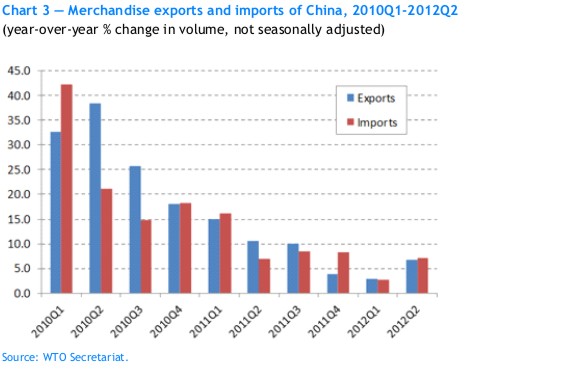

Chart 3 shows year-on-year growth in China’s

merchandise trade flows in volume terms (not seasonally adjusted), which have

declined steadily over the last two and a half years. Export growth dropped to

2.9% and import growth fell to 2.8% in the first quarter of 2012 before

rebounding slightly in the second quarter, but available monthly data suggest

that the third quarter results may be weaker still.

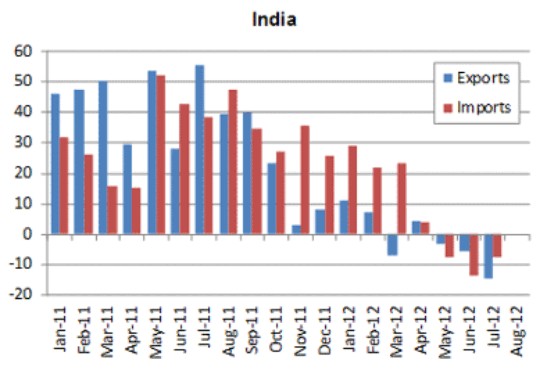

Year-on-year growth in monthly

merchandise exports and imports for selected economies in current dollar terms,

including partial data for the third quarter. Those

economies that have already reported figures for August show either stagnation

(e.g. China) or decline (e.g. Brazil, Japan, Singapore), which suggests

that that the recent weakness of trade will persist into the third quarter.