Global Trade Faces Setback Amid Rising

Tariffs

[ABS News Service/17.04.2025]

The

WTO Secretariat’s latest Global Trade Outlook and Statistics report, issued on 16

April, comes at a time of growing uncertainty for the global economy – and with

it, a sharp deterioration in the prospects for world trade.

Following

a strong performance in 2024, global trade is now facing headwinds from a surge

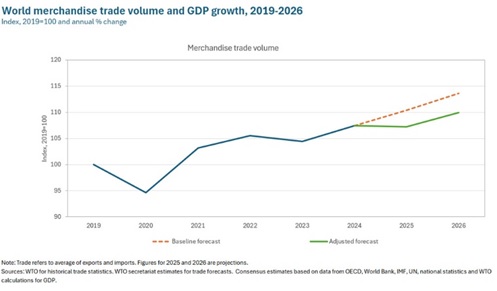

in tariffs and rising trade policy uncertainty. The volume of world merchandise

trade is projected to decline by 0.2 per cent in 2025 – almost three percentage

points lower than it would have been without the recent policy shifts. A modest

recovery of 2.5 per cent is expected in 2026.

This

marks a notable reversal from forecasts earlier this year, when WTO economists anticipated

continued trade expansion, supported by improving macroeconomic conditions.

There

are also important downside risks that could lead to a steeper decline in world

trade. These include the possible implementation of the currently suspended "reciprocal

tariffs" by the United States, as well as the potential for a broader spillover of trade policy uncertainty to other trading relationships.

If

enacted, reciprocal tariffs would reduce global merchandise trade growth by an additional

0.6 percentage points. A wider spread of trade policy uncertainty could cut growth

by a further 0.8 percentage points. Taken together, these risks would lead to a

1.5 per cent decline in world merchandise trade volume in 2025.

The

impact of recent trade policy changes varies sharply across regions.

According

to our current forecast, North America now subtracts 1.7 percentage points from

global merchandise trade growth in 2025, turning the overall figure negative. Asia

and Europe continue to contribute positively but less than in the baseline "low

tariff" scenario, with Asia’s contribution halved to 0.6 percentage points.

Meanwhile, the combined contribution of other regions – Africa, the Commonwealth

of Independent States (CIS), the Middle East, and South and Central America and

the Caribbean – also declines somewhat but remains positive. An important driving

force behind these changes is the decoupling between China and the United States,

resulting from tariffs that now well exceed 100 per cent.

The

disruption in United States–China trade is also expected to trigger significant

trade diversion, raising concerns among other markets about increased competition

from China. As trade is redirected, Chinese merchandise exports are projected to

rise by between 4 and 9 per cent across all regions outside North America. At the

same time, US imports from China are expected to fall sharply in sectors such as

textiles, apparel and electrical equipment, creating new export opportunities for

other suppliers able to fill the gap. This could open the door for some least-developed

countries to increase their exports to the US market.

Services

trade, while not directly subject to tariffs, is also expected to be adversely affected.

Declines in goods trade are likely to reduce demand for related services, such as

transport and logistics, while broader uncertainty is likely to dampen discretionary

spending on travel and to slow investment-related services.

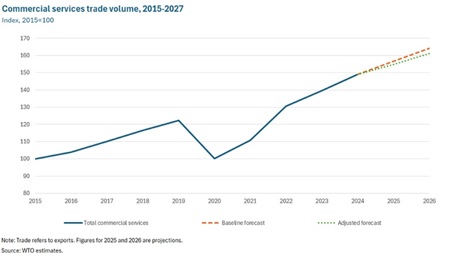

As

a result, the volume of global services trade is now forecast to grow by 4.0 per

cent in 2025 and 4.1 per cent in 2026 – well below the baseline projections of 5.1

per cent and 4.8 per cent. These figures are part of a new element in our analysis:

for the first time, this report includes projections for commercial services trade

in volume terms, complementing our long-standing merchandise trade estimates.

The

broader economic picture is also affected. World GDP is now expected to grow by

2.2 per cent in 2025 – 0.6 percentage points below the baseline prediction – before

recovering slightly to reach 2.4 per cent in 2026. The largest impact will again

be in North America, where growth is projected to slow by 1.6 percentage points,

followed by Asia (down by 0.4 percentage points) and South and Central America and

the Caribbean (down by 0.2 percentage points).

While

reciprocal tariffs alone would have a limited effect on global GDP, a wider spread

of trade policy uncertainty could nearly double the projected GDP loss, bringing

it to 1.3 percentage points below the baseline scenario.

All

of this follows a notably strong year for trade. In 2024, the volume of world merchandise

trade grew by 2.9 per cent, and commercial services trade expanded by 6.8 per cent.

With global GDP growing 2.8 per cent at market exchange rates, 2024 was the first

year since 2017 – excluding the post-COVID-19 rebound – in which merchandise trade

growth outpaced GDP growth. In value terms, merchandise exports rose 2 per cent,

to US$ 24.43 trillion, and services exports increased by 9 per cent, to US$ 8.69

trillion, supported by strong global demand.

Although

the current outlook is challenging, it is worth recalling that the trajectory of

world trade will not be determined by any single economy or bilateral relationship.

Much will depend on how the broader international community responds. The fact that

87 per cent of global merchandise trade takes place outside the United States –

and that bilateral trade between the United States and China accounts for around

3 per cent – is a reminder of the importance of other trading relationships.

Open,

predictable and cooperative trade policies remain essential – not just for trade

itself, but for global economic resilience.