ICRIER Release Report to

Make Turmeric Global

·

Testing

and Multiple Standard by Official Barriers in Exports

Executive

Summary

Introduction

Known

as the 'Golden Spice of India', turmeric, due to its preventive, therapeutic

and curative properties, has been integral to Indian and many South Asian

cultures, cuisines, and traditional systems of medicine like Ayurveda and

Unani. It is commonly used as a condiment, dye, drug and key raw material for

the cosmetic industry, and in traditional medicine and religious ceremonies.

The turmeric market value was around USD 58.2 million in 2020 and is projected

to grow at a CAGR of 16.1 per cent from 2020 to 2028. Rising awareness of

curcumin's medicinal benefits has fuelled an increase in turmeric demand.

Consequently, in 2023, global turmeric trade was valued at USD 587 million,

with exports at USD 320 million. The export value increased by 13.56 per cent

between 2017 and 2023.

Known

as the 'Golden Spice of India', turmeric, due to its preventive, therapeutic

and curative properties, has been integral to Indian and many South Asian

cultures, cuisines, and traditional systems of medicine like Ayurveda and

Unani. It is commonly used as a condiment, dye, drug and key raw material for

the cosmetic industry, and in traditional medicine and religious ceremonies.

The turmeric market value was around USD 58.2 million in 2020 and is projected

to grow at a CAGR of 16.1 per cent from 2020 to 2028. Rising awareness of

curcumin's medicinal benefits has fuelled an increase in turmeric demand.

Consequently, in 2023, global turmeric trade was valued at USD 587 million,

with exports at USD 320 million. The export value increased by 13.56 per cent

between 2017 and 2023.

Turmeric

is produced in various regions, such as Africa (Tanzania, Nigeria, and

Ethiopia), Asia (China), South Asia (India, Bangladesh, Sri Lanka, Myanmar) and

South America (Brazil, Peru), with these regions also being the largest

consumers. Emerging markets like the United States of America (USA) and the

European Un ion (EU) are rapidly adopting turmeric for nutraceuticals and food

applications, especially after COVID-19, as consumers seek healthier options.

India, as the leading producer, consumer and exporter, accounted for 73.40 per

cent of global production in FY 2022-23. India's export value rose from USD

182.53 million (2017) to USD 212.65 million (2023). The de mand for

high-curcumin and organic varieties of turmeric has also been rising because of

its diverse end-uses and affordability. Developed markets like the EU and the

USA are emerging as key hubs for high-quality turmeric that meets stringent SPS

and quality standards. In this context, India can become a turmeric pro

duction hub and widen its consumer base by expanding exports to destination

countries other than South Asia.

Overview

of the Turmeric Sector in India vis-a-vis Global Turmeric Sector

In

2022, global turmeric exports reached 238.81 thousand tonnes, up from 157.68

thousand tonnes in 2017. Turmeric exports peaked in 2020, reflecting a surge in

demand for curcumin-based products during the COVID-19 pandemic.

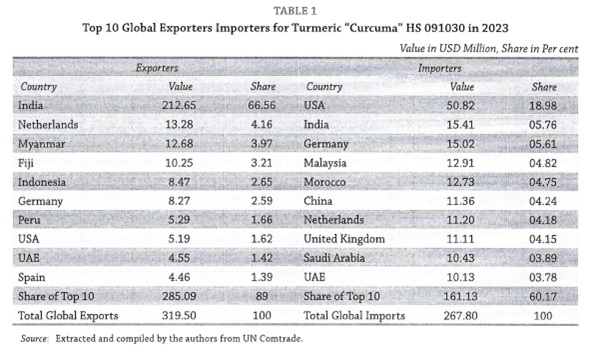

India,

being the largest producer and exporter, has solidified its market dominance by

increasing its export value from USD 182.53 million in 2017 to USD 212.65

million in 2023 (see Table 1), with its global market share rising from 71.55

per cent to 73.40 per cent during the period.

The

overall production of turmeric in India in creased from 2012-13 to 2022-23,

with fluctuating trends. Demand and production rose after the pandemic, but

price fluctuation led to output fluctuation. Although there was an increase in

cultivated area, turmeric yield per hectare declined by a CAG R of approximately

3.24 per cent between 2012-13 and 2022-23.

This

reflects the challenge of maintaining yield efficiency.

According to the Ministry of

Agriculture and Farmers ' Welfare 2024 (Third Advance Estimate of FY 2023-24),

297,460 hectares of land is under turmeric cultivation in India, with an

expected production of 1, 041, 730 MT.

As

the Government of India aims to make India the global turmeric production hub,

the Ministry of Commerce and Industry projects that India's turmeric exports

will reach USD 1 billion by 2030.

- State-wise Turmeric Production

Between

2012-13 and 2022 -23, India's turmeric production and cultivation across states

has undergone significant changes. Maharashtra, Telangana, Tamil Nadu,

Karnataka, Madhya Pradesh, Andhra Pradesh and Odisha are some of the top

turmeric-producing states. While Gujarat, Haryana, and Manipur have dropped out

of the top 10 turmeric producing states, Maharashtra and Odisha have emerged as

key producers as of 2022-23. Over 30 varieties of turmeric are cultivated in

India across more than 20 states, with both local and improved varieties

developed by agricultural research institutions.

Local

varieties possess certain qualities and characteristics based on the specific

geographical location. These varieties vary in curcumin content, yield and

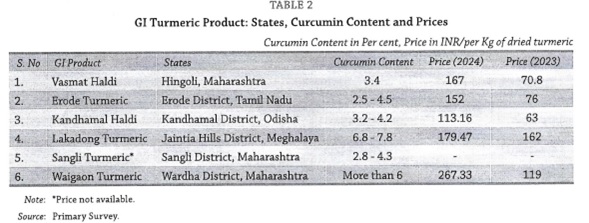

disease resistance. To protect and promote the reputation and unique ness tied

to the respective region, they get a geographical indication (GI) tag. India

has six GI tags for turmeric (see Table 2).

To

maintain India's global dominance, it needs to evolve from being just a raw

turmeric supplier by innovating, ensuring quality, and adopting sustainable

practices. Several companies have already taken strides in this direction and

produce curcumin extracts for pharmaceuticals and nutraceuticals. Products like

Vicco Turmeric Cream merge turmeric with modern cosmetics, linking Ayurvedic

traditions with contemporary personal care. High-curcumin variants like

Alleppey and Lakadong turmeric are gaining international attention for their

medicinal benefits.

Methodology

The

study is based on secondary data and information analysis, and a primary survey

of diverse stakeholders in the turmeric value chain. The stakeholder s included

farmers, farmer producer organisations (FPOs), companies, certification

bodies, laboratories, government agencies, and non-governmental organisations

(NGOs) across six states, namely Telangana, Tamil Nadu, Maharashtra, Meghalaya,

Odisha, and Madhya Pradesh. There were two stake holder consultations,

multiple case studies and key informant interviews, and a semi-structured

questionnaire -based survey, ensuring a comprehensive representation of the

perspectives of over 500

stakeholders.

Key

Findings of the Primary Survey

The

semi-structured questionnaire-based sur vey covered 262 farmers, 45 FPOs, and

69 companies engaged in the turmeric value chain.

-

Farmer Survey

The

survey revealed that most turmeric farmers (80 per cent) earned less

than 50 per

cent of their annual income from turmeric. This is largely due to their

reliance on cultivating multiple crops like paddy, soybean, maize, sugarcane,

and cotton.

The decline in turmeric production

in recent years is due to fluctuating prices and gaps in market access,

highlighting the need for targeted support to stabilise turmeric cultivation.

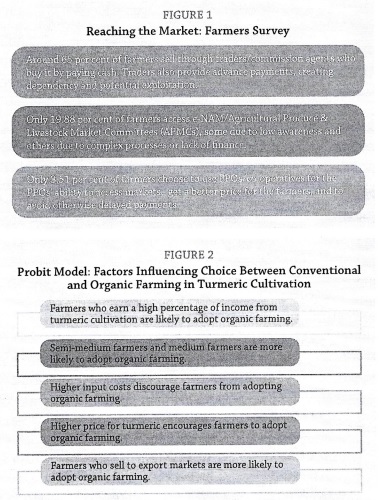

Farmers

also reported a decline in turmeric cultivation in the last three years,

stating several reasons, like a sudden fall in prices, inadequate

infrastructure, unfavourable weather conditions, pest infestations, inability

to connect to the right buyers and issues related to soil fertility. Some other

findings are given in Figure 1.

Farmers are either

conventional farmers or organic farmers. Organic farmers can be (a) default

organic/natural, (b) third-party certified organic farmer under National Pro

gramme for Organic Production (NPOP) of Agricultural and Processed Food

Products Export Development Authority (APEDA), and (c) self-certified under the

Participatory Guarantee System of India (PGS-India) of the National Centre of

Organic Farming (NCOF).

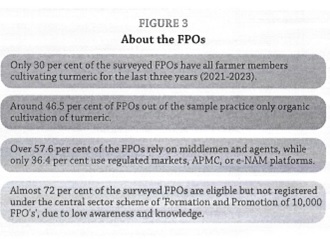

A

probit model was used to identify the primary determinants that influence the

farmer's choice between conventional and organic farming in turmeric

cultivation.1 The dependent variable is a binary variable representing the

choice of farming method adopted by a turmeric farmer. The key findings are

presented in Figure 2.

While

the farmland holding varies across states, most turmeric farmers in India are

small and marginal farmers. There are state-wise differences in farming

methods, reflecting the state's socio-economic and institutional dynamics. For

example, turmeric farmers in Meghalaya practice co-operative farming, while

farmers in Tamil Nadu, Madhya Pradesh, Maharashtra, and Odisha are either doing

their own farming or contract farming. These farmers highlighted the following

multiple benefits of contract farming:

·

Security and support in

agricultural practices from companies

·

Access to quality seeds, fertilisers

and other inputs, reasonable pricing and reduced risk exposure

·

Training and knowledge sharing

like free integrated pest management (IPM) kits

·

Guidance on efficient

fertiliser application to help optimise crop yield and quality.

Various

factors, including curcumin content, market demand, and GI, influence the

market price of turmeric. For example, in Meghalaya, the Lakadong variety is

renowned for its high curcumin content, market value, and GI tag. In 2024, this

variety sold at an average price of INR 32.14 per kilogram for raw turmeric,

while its dried and powdered forms fetched INR 179.47 per kilogram and INR

266.66 per kilogram, respectively. The Erode Manjal variety, GI-tagged but with

lower curcumin content ranging from 2.5 to 4.5 per cent, sold for INR 152 per

kilo- gram for dried turmeric in 2024 (see Table 2).

Furthermore,

global value chains are reshaping themselves as consumer demand shifts to

wards organically cultivated turmeric with high curcumin content. Although

organic turmeric fetches a higher price in the market, the transition from

conventional to organic farming is often a rigorous and expensive process. This

creates financial strain and uncertainty for farmers, discouraging them from

making the switch.

Enhancing finance, marketing,

co-operatives, and regulated market access is essential to empower farmers and

boost output

-

FPO Survey

The

survey highlighted the essential support FPOs offer to farmers, especially

small and marginal ones (over 80 per cent of FPO members), by providing inputs,

post-harvest processing, aggregation, marketing and better price negotiations.

Some key findings are presented in Figure 3.

FPOs

attributed the decline in turmeric production to frequent market price

fluctuations. De spite government assistance to FPOs through different schemes

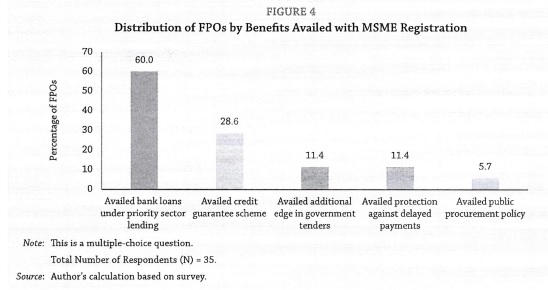

at both the central and state levels, the number of FPOs registered and re

ceiving assistance under the schemes was less than 10. Most of the surveyed

FPOs, registered as MSMEs, receive several benefits, as shown in Figure 4.

FPOs need comprehensive support to bolster

their operations, expand their market reach, and boost their overall

sustainability.

However,

they continue to face the following constraints:

i. Market linkages and information/knowledge

gap

ii. Visibility to buyers since they are not

listed under spices or turmeric on government portals

iii.

Getting credit and accessing benefits/ subsidies.

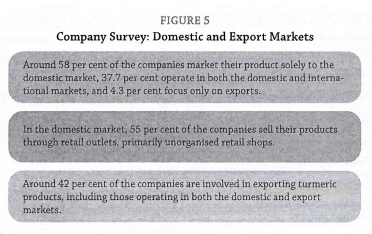

- Company Survey

The

surveyed companies encompass manufacturers, wholesalers, exporters, retail and

contract farming companies, and companies handling turmeric products (whole

turmeric, turmeric powder and turmeric extracts). Some of the key findings of

the company survey are presented in Figure 5.

Companies

source turmeric through multiple channels, including farmers, FPOs, organic

clusters, e-NAM, regulated market s and traders, with over 50 per cent of the

companies re lying on mandi agents,

commission agents and local traders, sourcing both organic and conventional

turmeric.

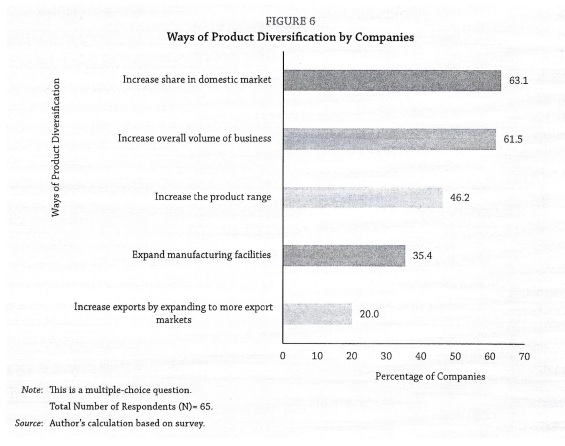

With

an expected growth rate of more than 15 per cent, the companies also intend to

diversify their turmeric portfolio in the next five years (see Figure 6).

The

survey highlighted that the use of turmeric has expanded globally, with foreign

firms sourcing turmeric from India and Indian firms growing internationally.

Some

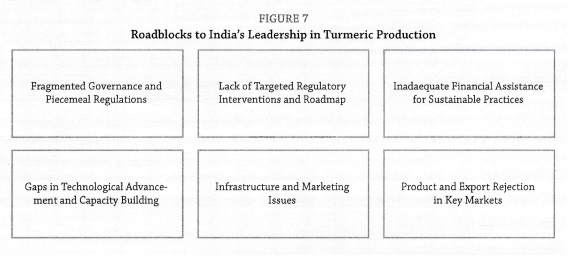

Roadblocks to India's Leadership in Turmeric Production

Despite

holding a commanding share exceeding 62 per cent of global turmeric trade,

India faces challenges that impede further growth, ranging from the rejection

of spices in key export markets to price fluctuations leading to farmers

withdrawing from the cultivation of turmeric to not meeting the desired

curcumin levels re quired by companies (see Figure 7).

We

are only able to supply 10 per cent of turmeric products with the high curcumin

content required by global clients. Fragmented supply chains, lack of uniform

quality of produce, lack of access to high-quality inputs, gaps in testing and

certification, lack of traceability, targeted subsidies and support, and

infrastructure gaps are some of the issues that stem from the complex institutional

structure for governance. With varying end-uses of turmeric, there exist

multiple organisations, each with its own regulations, policies and governance,

depending on end-use and production. There are different regulatory bodies for

domestic markets and exports. Multiple agencies, such as the Spices Board

India, APEDA, Food Safety and Standards Authority of India (FSSAI) and Bureau

of Indian Standards (BIS), set standards for agricultural produce. The Spices

Board India looks at processed turmeric, while APEDA covers fresh turmeric.

Each of these agencies have onboarded different laboratories and ask for

different compliance requirements. Additionally, although domestic turmeric may

align with international standards such as the CODEX Alimentarius, it is low on

curcumin (2 per cent), which does not meet the global demand for turmeric

varieties of high curcumin content (5 per cent or more). We do not have mutual

recognition agreements with key markets for processed organic produced.

Globally,

rising consumer awareness regarding food safety and standards has resulted in

strict er border review processes and requirements in export partners.

Recently, border refusals of Indian spices have become more frequent and

non-compliance with safety standards has become a major issue. Instances of

adulteration in turmeric by manufacturers seeking to profiteer by using

low-cost raw materials and additives have also resulted in the rejection of

turmeric by global buyers.

Pathways

to a Resilient Future: How Can India Retain its Leadership Position and Move up

the Value Chain?

The

Government of India is aware of the issues, and the Honourable Prime Minister

announced the setting up of the National Turmeric Board to resolve some of the

issues related to regulatory gaps, quality and standards, research and product

development, etc. Establishing a single nodal agency like the National Turmeric

Board can ensure quality standards, traceability and streamline certification

and testing processes. Once the domestic quality and standards are in order,

signing mutual recognition agreements for standards and certification for both

fresh and processed turmeric with key export markets can reduce the compliance

burden and enhance trade. Subsidies should be linked to help develop high -end

product value chains. For example, there can be subsidies for third -party

certification, cultivation of high curcumin varieties, research and development

(R&D) for value-added turmeric products and for promoting GI products.

Investments in post-harvest infrastructure, scaling up turmeric FPOs and

fostering knowledge sharing through R&D and global collaborations are

crucial for maintaining competitiveness.

Promoting

high-curcumin varieties and leveraging international platforms can solidify

India's position as a leading turmeric exporter.

To

help India retain its leadership position, it is urgent to replicate the

different collaborative models and best practices discussed in this re port.

Collaborative platforms involving policymakers, traders, corporations and

processors are instrumental in developing effective strategies. Industry events

such as the World Spice Congress and Global Turmeric Conference pro vide

valuable opportunities for knowledge sharing, networking and identifying market

trends. International platforms such as these can also be used to market India

's success in turmeric, as well as disseminate information about importing

country requirements. Capacity building for farmers, processors and exporters

can significantly enhance the industry's global competitiveness. By aligning

production practices with international benchmarks and fostering a

collaborative ecosystem, India can solidify its position as a reliable and

preferred supplier of high quality turmeric in the global market.